TrumpCare Death Spiral Watch: Molina may jump ship over GOP-induced uncertainty

Tue, 01/24/2017 - 11:20pm

Politically, the big unknown is whether or not Paul Ryan and Mitch McConnell will get away with trying to pin the blame for this on the Democrats/the law itself. That's why they've been pushing the "Obamacare is already in a death spiral!" claim hard for the past few weeks, even though it quite simply isn't.

...So, if this does end up in a worst-case scenario, Trump's "stop enforcing the mandate altogether!" order here could end up causing that death spiral even if the GOP doesn't technically end up repealing anything legislatively. The carriers would start announcing that they're bailing next year as soon as this spring (remember, the first paperwork for 2018 exchange participation has to be filed in April or May), and McConnell/Ryan would simply say, "See?? We told you it was collapsing all by itself! We didn't touch nuthin'!!"

The agencies also estimate net federal subsidies for coverage obtained through the marketplaces to be $49 billion, or 0.3 percent of GDP, in fiscal year 2017. Those subsidy amounts are projected to rise at an average annual rate of about 9 percent, reaching $110 billion (or 0.4 percent of GDP) in 2027. For the 2018– 2027 period, the net subsidy is projected to total $919 billion under current law.

...Finally, the CBO is now stating, flat out, that prior to Trump taking office, the GOP starting the ACA repeal process, Trump's "sabotage" executive order and so forth, they were projecting average subsidies for ACA exchange enrollees to increase at a rate of roughly 9% per year for the next decade.

...Again, this is all speculative, but the bottom line is that the CBO is stating pretty clearly that with the ACA, while they don't see the individual market being in the greatest shape, neither do they see a death spiral under the current law.

October 6, 2016, via Anna Wilde Mathews:

Molina Outperforms Rivals in ACA Marketplaces

...Molina’s approach—rigorous cost control, limited networks of doctors and hospitals and close management of patients’ health—signals what can work in the health-coverage marketplaces created by the Affordable Care Act. Long Beach, Calif.-based Molina has done relatively well in the exchanges, where larger rivals have faltered. While UnitedHealth Group Inc., Aetna Inc. and Humana Inc., have lost millions on ACA plans and are pulling back from the marketplaces, Molina is profitable, though the margins are slim. The company projects that its margins on the exchange business this year will be within its targeted range, between 1.5% and 2%.

...Analysts worry that Molina, which has around 600,000 marketplace enrollees across nine states, next year may pick up high-cost enrollees formerly covered by insurers that withdrew from exchanges. Molina “is really going to be tested as the bigger players leave the market and the risk moves to them,” said James Sung, an associate director with S&P Global Ratings.

Ms. Rubino said company officials “anticipate another solid year” for the exchange business in 2017, and that Molina adjusted prices to account for the impact of others’ exits.

So, that was how Molina, one of the largest ACA exchange participants (around 7% of all exchange enrollees) felt about the future of the ACA just a month before the election.

How about today?

Tuesday, January 24th, via Bob Herman of Axios:

In an interview, Molina said the executive order is "symbolic" and doesn't change the plans for his company, an insurer that mostly covers Medicaid members but also has more than a half million Obamacare customers. Yet when asked if Molina Healthcare would keep offering Obamacare plans in 2018, he said: "There are just too many unknowns at this point to give a definitive answer."

Why this matters: Insurance companies need to submit their 2018 Obamacare plans and rates in the next few months. Molina is a significant and profitable player in the marketplaces, and its hesitancy indicates insurers will wait as long as they can before they decide to stay in or leave. That's not exactly a recipe for a stable market.

On Obamacare: Trump cannot unilaterally eliminate Obamacare's insurance mandate and coverage penalties. They are embedded within the law and require an act of Congress. Instead, Molina is more concerned what Congress will offer up as a full-scale replacement.

Yup. It's true that some carriers might have been considering dropping out of the exchanges in 2018 regardless...but between Trump winning, the GOP going full-speed ahead with repeal plans, Trump's executive order, the GOP not having the slightest clue what, if anything, they would replace the ACA with (or when that might take place), and the initial filing deadlines bearing down on the carriers like a freight train, some of the major players are already seriously talking about bailing because of all the additional uncertainty.

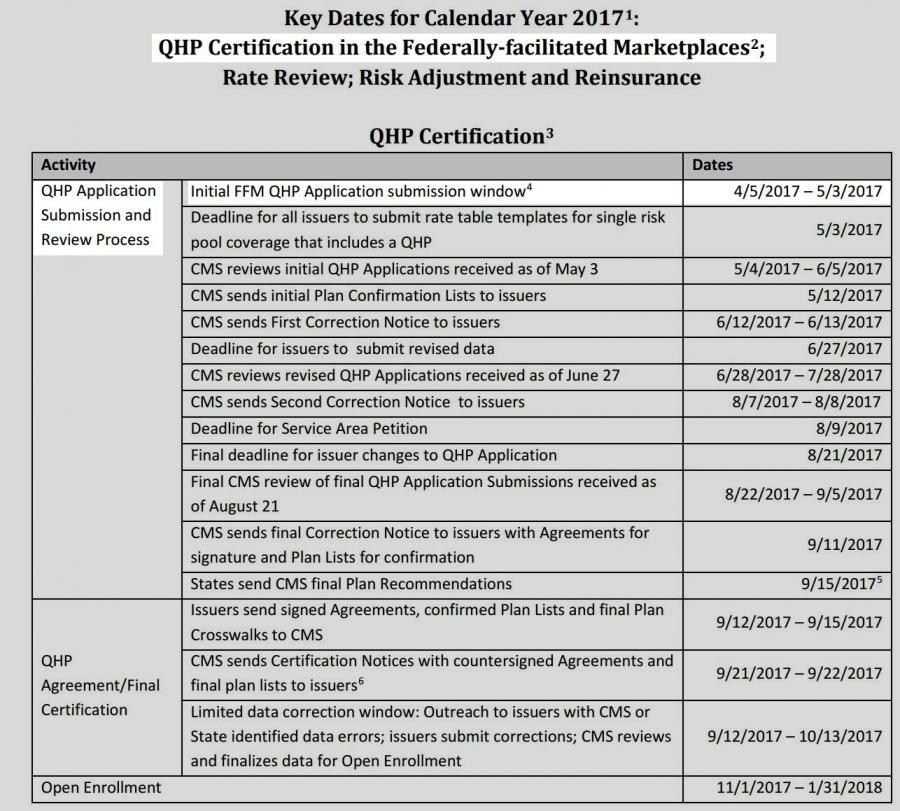

And for the record, here's the official timeline for carrier participation on the federal exchange (I presume the dates are a bit different for the various state-based exchanges, but we're still talking about just a few months here):

Advertisement