Well, what do you know? HHS confirms: Millions of OFF-exchange enrollees may qualify for subsidies!

Tue, 10/04/2016 - 11:36am

Some Guy, September 8th, 2016:

Until now, I've been assuming that the vast majority--say, 99% or so--of those 7.1 million people who are enrolled in individual plans directly thorugh the carriers must be over 400% FPL, undocumented immigrants, have some other type of legal issue preventing them from enrolling on the exchanges, etc. etc.

HOWEVER, if McKinsey's statement above is accurate, this isn't the case at all.

Why? Because if 69% of the entire individual market (including GR/TR enrollees) is eligible for subsidies, that has to mean that some percentage of off-exchange enrollees are...and not just people in transitional/grandfathered plans.

- The total market is 20.2 million people.

- 69% of that is appx. 12.9 million people McKinsey says are eligible for APTC.

We can account for 9.4 million of those, of course; those are the 9.4 million who are receiving APTC via exchange policies.

Subtract those, and you have another 3.5 million people eligible for APTC assistance out of the 9.1 million total off-exchange enrollees (ACA, GR & TR).

Since there only appear to be about 2 million GR/TR enrollees, that means that at least 1.5 million people enrolled in off-exchange ACA-compliant polices would actually be eligible for subsidized coverage if they were to enroll in the exact same policies (or similar ones) through the exchange.

HHS Report, October 4th, 2016:

New analysis shows 2.5 million Americans currently buying individual health coverage off-Marketplace may be eligible for Affordable Care Act premium tax credits

HHS encourages consumers to evaluate Marketplace options during upcoming Open Enrollment

Since the Affordable Care Act became law, millions of Americans gained coverage or found more affordable options thanks to premium tax credits available through the Health Insurance Marketplace. Today, the U.S. Department of Health and Human Services (HHS) released data showing that 2.5 million Americans who currently purchase off-Marketplace individual market coverage may qualify for tax credits if they shop for 2017 coverage through the Marketplace. Six states (California, Texas, Florida, North Carolina, Illinois, and Pennsylvania) each have more than 100,000 individuals enrolled in off-Marketplace individual market coverage whose incomes may qualify them for Marketplace tax credits.

“More than 9 million Americans already receive financial assistance through the Health Insurance Marketplace to help keep coverage affordable, but today’s data show millions more Americans could benefit,” said Secretary Sylvia M. Burwell. “We encourage everyone to check out their options on HealthCare.gov or their state Marketplace and see if they qualify for financial assistance. Marketplace consumers who qualify for financial assistance usually have the option to buy coverage with a premium of less than $75 per month.”

Today’s analysis estimates that about 6.9 million individuals currently purchase health insurance in the off-Marketplace individual market. Of those, about 1.9 million either have incomes that would qualify them for Medicaid or place them in the Medicaid coverage gap or are ineligible to purchase Marketplace coverage due to immigration status, while the remainder could enroll in Marketplace qualified health plans (QHPs).

I'm not sure whether that 6.9 million off-exchange estimate (18 million total) includes grandfathered/transitional policies or not. The actual ASPE report makes no mention of/reference to gf/tr plans one way or the other. If the 18 million figure doesn't include them, that means that my estimate (appx. 7 million off-exchange ACA-compliant enrollees) is dead on target. If it does include them, then the ACA-compliant portion is likely a couple million people lower.

I haven't actually read through the ASPE report yet; I'll update/clarify later if If find out the answer to this.

Counting both Marketplace and off-Marketplace consumers, more than 70 percent of all QHP-eligible individuals currently insured through the individual market have incomes that could qualify them for tax credits. If the Marketplace-eligible uninsured are included as well, today’s analysis indicates that almost 80 percent of all Americans eligible for Marketplace coverage could qualify for tax credits based on their income.

Many consumers remain unaware of the financial assistance available to them through the Marketplace. For example, a recent Commonwealth Fund survey found that only 52 percent of uninsured adults were aware that financial assistance is available through the Marketplaces.

Whether you support the ACA or oppose it, this is a stunning figure. Half the uninsured still don't know about the tax credits? I'm not saying I expect everyone to know how it works or the exact numbers involved, but to not even be aware that financial assistance is available at all, 6 years after the law was signed, is amazing.

Tax credits available through the Marketplace are designed to both improve affordability and protect consumers from the impact of rate increases. Consumers may be eligible if their incomes are between 100 and 400 percent of the federal poverty level (about $100,000 for a family of four). If all premiums in an area go up, the large majority of Marketplace consumers will not have to pay more because tax credits will increase in parallel. A recent HHS analysis found that, in a hypothetical scenario where all 2017 rates increased by 25 percent, 73 percent of current Marketplace consumers would be able to purchase coverage for less than $75 per month thanks to tax credits.

During the upcoming Open Enrollment, HHS will be placing new emphasis on making sure people currently buying individual market coverage off-Marketplace know their options. For example:

- For the first time, our decisions about where to target our outreach efforts – from regional TV and radio to search and digital marketing – will be based in part on where we can reach these consumers, supplementing our continued use of data to target the remaining uninsured.

- We are strengthening our relationships with agents and brokers. Agents and brokers are a critical channel for reaching off-Marketplace consumers, who often purchase coverage with the help of an agent or broker. Changes this year, such as offering agents and brokers new Marketplace training tools and faster registration, will make it easier for agents and brokers to enroll people in Marketplace plans. Improvements to agent and broker education and resources will ensure that they and their customers know all their options.

- We are working with issuers to provide consumers with more and better information about the Marketplace. This includes updating standard notices to make them shorter, simpler, and more user friendly.

- We are making it easier for issuers to facilitate transitions from a parents’ plan into the Marketplace. Specifically, recent guidance from the Department of Labor makes clear that the sponsors of employer plans can – and are encouraged to – provide additional information that will help young adults understand their options and enroll in Marketplace coverage as appropriate.

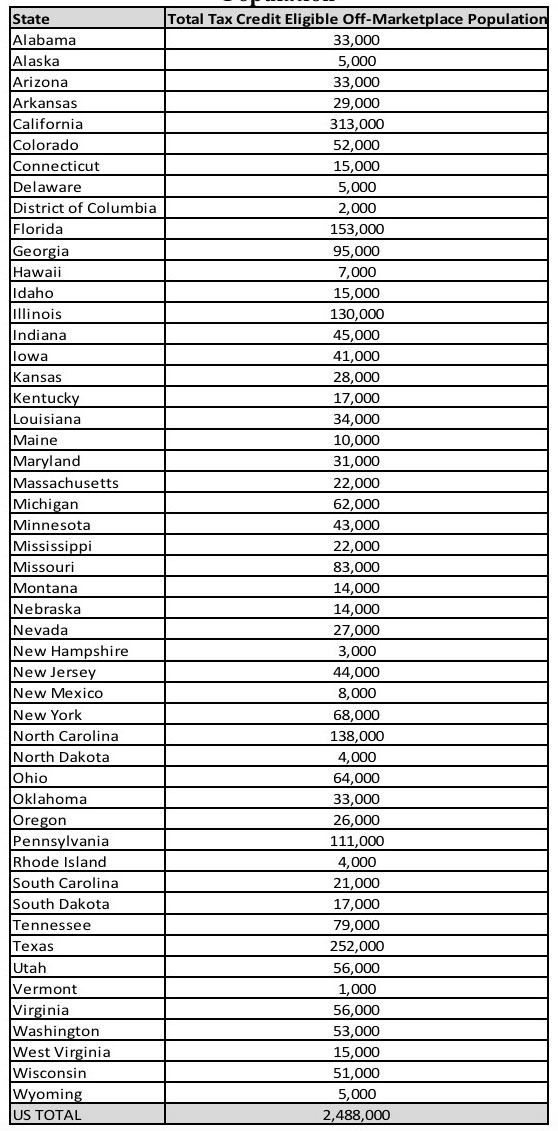

They even provide a state-by-state breakdown table showing their best estimates of the number of people enrolled in off-exchange individual policies who would likely be eligible for financial assistance (APTC and, in most cases, CSR as well) in each state:

UPDATE: OK, this is even better...reading over the ASPE report, it appears that I might have even helped inspire the ASPE to conduct this analysis in the first place:

Another group that could be affected by premium changes are people who purchase coverage through the individual market, but not through the Health Insurance Marketplace. Less is known about this group than about Marketplace consumers or the remaining uninsured. Even estimates of the total number of people with off-Marketplace coverage vary, ranging from about 5 to 9 million.v Importantly, tax credits are not available for coverage purchased off-Marketplace because a central function of the Marketplace is determining eligibility for financial assistance.

- v: Federal Subsidies for Health Insurance Coverage, Congressional Budget Office, March 2016

- Survey of Non-Group Health Insurance Enrollees, Kaiser Family Foundation, May 2016

- Mark Farrah Associates, The Unpredictable Individual Health Insurance Market

- Charles Gaba Guess what? Several million OFF-exchange enrollees appear to qualify for exchange subsidies!!, September 8, 2016

Advertisement