Colorado: *Approved* avg. 2017 rate hikes: 20.4% (Sm. Group: 2.1%)

Tue, 09/20/2016 - 1:49pm

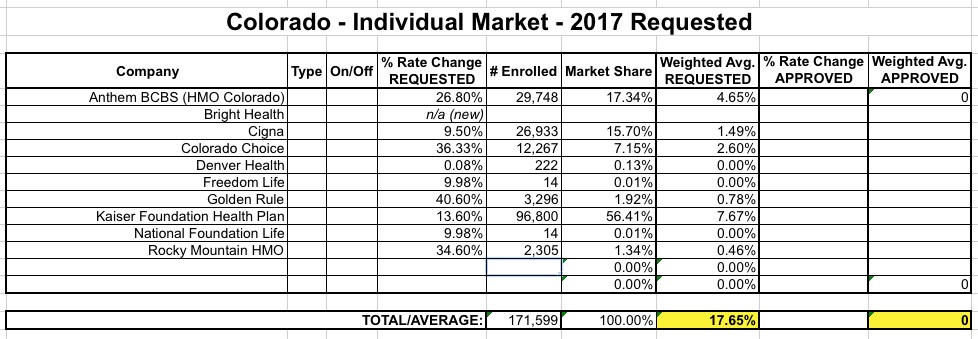

Things have actually been relatively quiet on the Colorado rate hike news front since June, when I first ran my projected estimates of requested rate changes for the 2017 individual market:

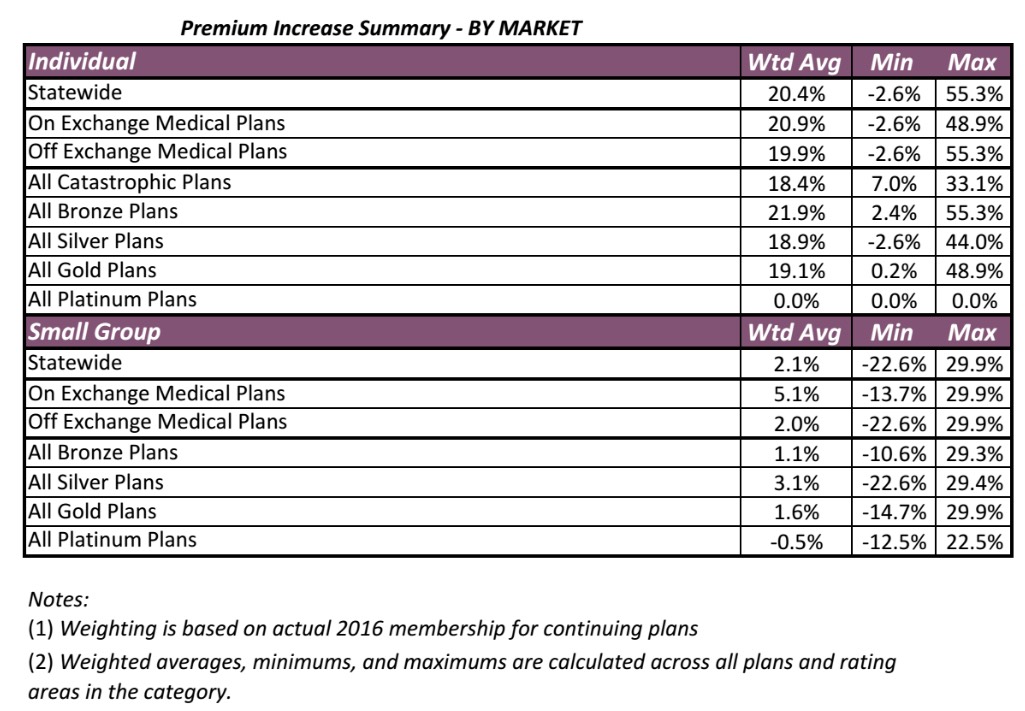

Well, today the Colorado Dept. of Insurance released their approved rate hikes for both the individual and small group markets. Unfortunately, I don't see an actual carrier-by-carrier breakout, but they do provide weighted averages by other criteria such as metal level, on exchange vs. off exchange and so on:

While it would be nice to have the averages weighted by carrier, the on/off breakout is kind of interesting because it also lets me know what the relative numbers are between the two. For the individual market, note that the on exchange weighted average is 20.9% vs. the off-exchange's 19.9%.

Since the overall average is 20.4%...which falls exactly in between the two, this suggests that exactly 50% of Colorado's ACA-compliant individual market is on the exchange, plus another 50% off-exchange, which I admit sounds suspicious. Anyway, the 20.4% approved average is, sadly, 2.8 percentage points higher than what I had estimated the requested average to be.

On the small group side, it's just 2.0% for the off-exchange market and 5.1% for on-exchange...but the overall average is just 2.1%, so the vast majority of sm. group enrollees are off exchange in Colorado, which makes sense since the ACA's SHOP program hasn't had much of an impact in most states.

The other noteworthy news here comes from an accompanying FAQ/Memo from the CO DOI:

How do the 2017 premiums compare to premiums in 2016?

Premiums are increasing for the individual market (not employer-based) in 2017 more than they did in 2016. On average, in the individual market, premiums are increasing by 20.4%. An individual’s age and location will impact their premium increase, making it lower or higher than the average.

The average increase also assumes a person stays with their current plan. Consumers can often lower an increase by shopping and comparing plans. For example, consumers who bought individual plans through Connect for Health Colorado, but who did not qualify for tax credits, can bring down their average increase in premium to around 13% if they switch to the lowest cost plan in the same metal tier. And consumers who qualify for premium tax credits may actually see lower subsidized premiums.

Note that such increases are not happening in the small group market where the average increase is 2.1%.

Will these be the premiums that consumers actually pay for health plans?

Yes, but these do not take into account consumers’ eligibility for the federal tax credits that help to reduce the cost of premiums. These tax credits, called Advance Premium Tax Credits or APTC, are only available if coverage is purchased through Connect for Health Colorado, the state’s health insurance exchange. Eligibility for the APTC is based on household income.

It is important to note that the average person who currently receives tax credits for their 2016 insurance, and who will enroll in the same plan for 2017, will actually see an average decrease of 11% for their subsidized premium, even though the actual premiums are increasing. And if those folks shop for a lower cost plan, they can reduce their subsidized premium even more, up to 29% on average.

Consumers can contact Connect for Health Colorado at www.connectforhealthco.com / 855-752-6749 for more information about APTC.

...Which carriers are leaving the individual market, and why are they leaving?

UnitedHealthcare and Humana Insurance will not offer individual plans in 2017. Anthem Blue Cross and Blue Shield will not offer its PPO (Preferred Provider Organization) individual plans, and Rocky Mountain Health Plans (RMHP) determined that it will reduce individual plan offerings for 2017, offering individual plans only in Mesa County, only via its Monument Health affiliate.

All of these companies will continue to offer their small and large group plans for employers.

These companies tried different products in the market, and some are now are pulling back what hasn’t worked. We’re seeing the free market at work within the private sector. It’s a market correction taking place on a national scale as insurance companies are still trying to figure out what to sell, how to sell, and how to price in the individual market. Some have figured it out, while others are stepping back to re-evaluate their approach.

Other companies are staying in the market, and a new company, Bright Health Plans, has applied to sell individual plans in Colorado, believing they have developed an innovative approach for delivering quality healthcare. Where some companies have experienced challenges, others see opportunities.

What’s the impact of those carriers leaving the individual market?

The carriers mentioned above who are departing the individual market, or scaling back their offerings, will impact about 92,000 consumers who will not be able to renew their 2016 plans for 2017.

- About 10,000 people from Rocky Mountain Health Plans

- 10,549 people from UnitedHealthcare

- 9,914 people from Humana Health

- 62,310 people from Anthem’s Blue Cross Blue Shield PPO division

...Do changing premiums impact the tax credits (Advance Premium Tax Credits or APTC)?

Yes. Because the calculation of the APTC is tied to premiums for the second-lowest silver plan available to a consumer, a change in the premium of that plan will impact the APTC. However, while the calculation is connected to that silver plan, consumers who qualify for an APTC can use the credit to shop for any bronze, silver, gold, or platinum plan available in their area through Connect for Health Colorado.

With premiums increasing, those eligible for the APTC will get more in tax credits to help them afford the higher premiums.

The tax credit amount is determined by subtracting the expected household contribution to medical premiums (based on household income) from the cost of the second-lowest silver plan (also called a benchmark cost) available. The expected contribution is determined on a sliding scale, established by the federal government. Below is the basic formula.

(2nd lowest silver plan premium in your area) – (your expected household contribution) = tax credit amount

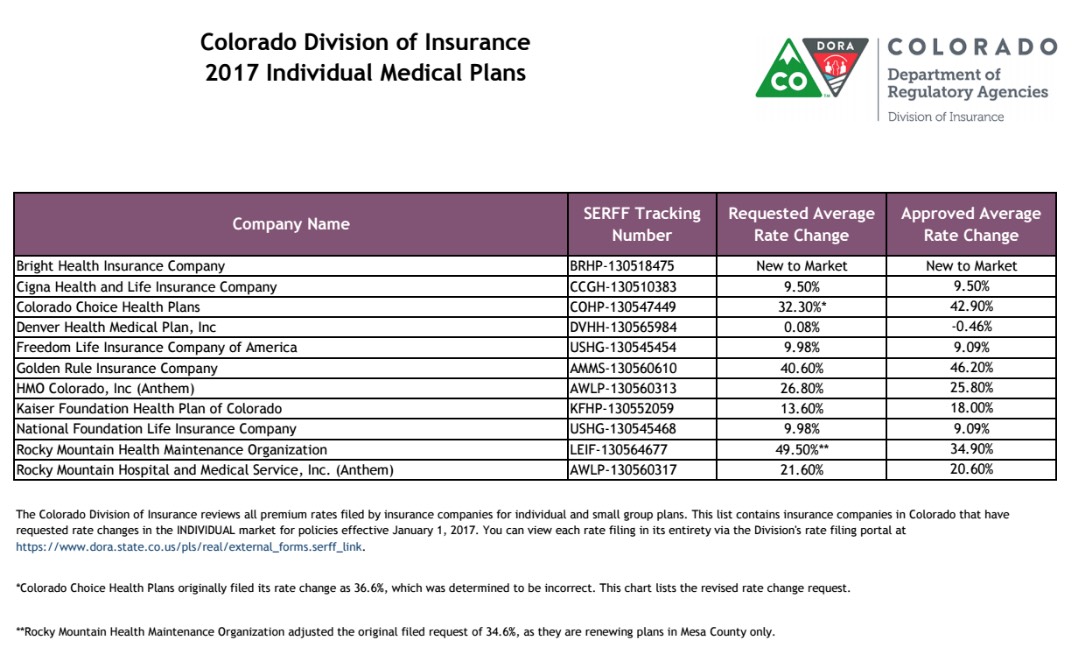

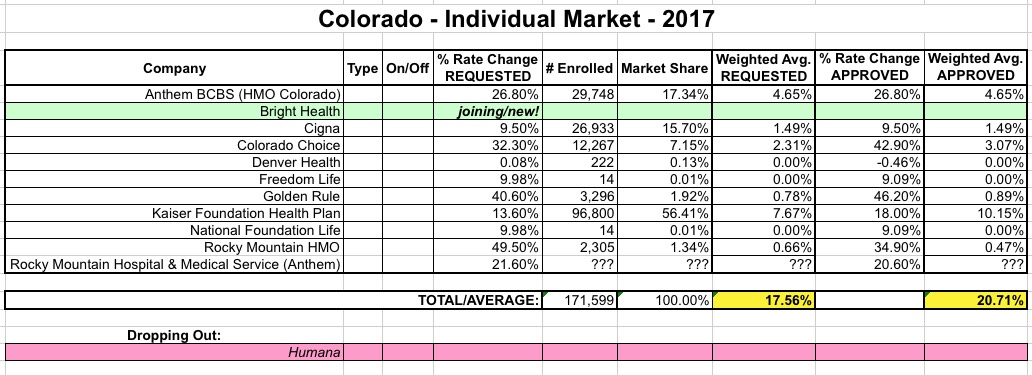

UPDATE: OK, thanks to Louise Norris for pointing me in the right direction to track down the actual individual carrier approved rate changes:

The "requested" rate percentages vary a bit from what I had in June, mainly due to some corrections and resubmissions, but when I plug everything in, the approved average is very close to the official 20.4% given by the state, so I had the market share ratios pretty close:

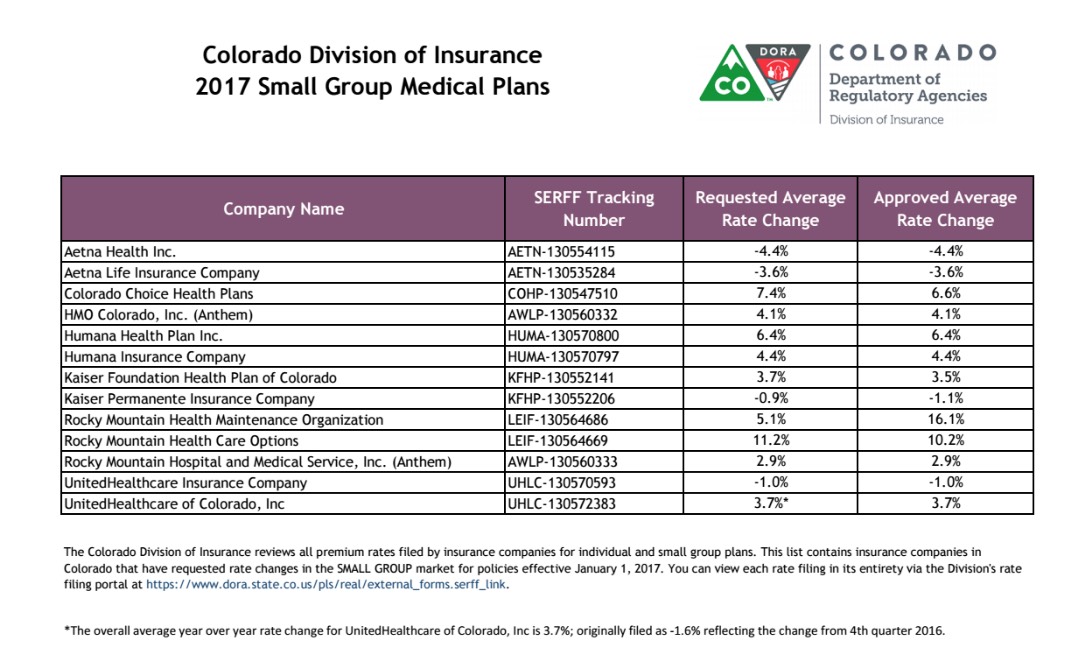

And here's the Small Group breakout, FWIW:

Advertisement