UPDATED: 2016 rates may not be so bad after all...as long as you shop around

Thu, 06/11/2015 - 10:33am

As I've noted over and over again, the headlines screaming about massive rate hikes in 2016 have to be taken with a massive grain of salt due to a whole mess of factors and variables. In some cases substantial increases are indeed likely, but in other cases the authors of the stories are flat-out lying.

In other words, be very careful to understand the context of the "rate increase" story before drawing any conclusions when reading reports of either "excessively high" or "quite reasonable-sounding" 2016 premium rate change requests.

With all of that in mind, healthcare consulting firm Avalere Health has released a new analysis of 2016 rate filings across 8 states, and the news is...pretty damned good, actually:

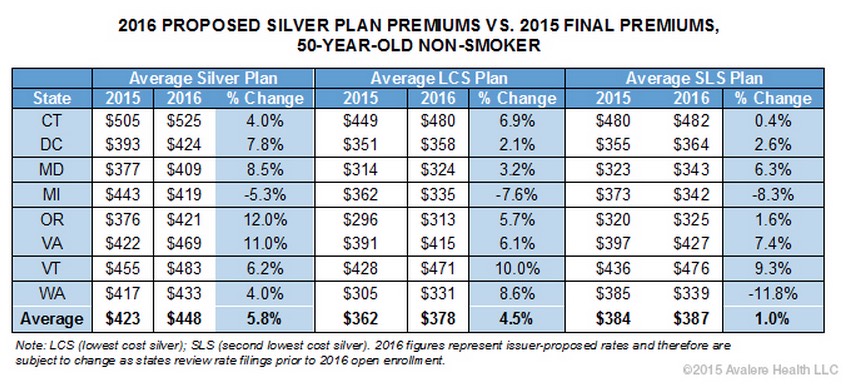

A new analysis from Avalere finds wide geographic variation in 2016 premium increases for individual market exchange plans, based on proposed rate filings in eight states where complete data is available.

Specifically, premiums for silver plans will increase 5.8 percent on average across the states analyzed, ranging from a 12.0 percent average increase in Oregon to a 5.3 percent decrease in Michigan. More than two-thirds (68 percent) of 2015 exchange enrollees picked silver plans.

“While recent public attention has focused on a subset of plans that filed for premium increases of 10 percent or more, these data reveal that most plans are proposing more modest increases,” said Caroline Pearson, senior vice president at Avalere. “Notably, final premiums could be even lower than those proposed.”

Again, there's a lot of caveats crammed in there:

- It only covers 8 states (well, 7 states plus DC), with a combined total population of potential individual market enrollees of around 3.1 million out of 28 million

- It only covers the Silver plans in those states...although those are the plans chosen by around 2/3 of all enrollees, and Silver plans also include Cost Sharing Reduction options

- Again, these are requested changes only; they could drop even further when finalized

Even so, this is a good example of why, as I said last month: DON'T PANIC.

However, the most important factor here is that for most people, keeping the rates low (or at least reasonable) will rely heavily on making sure to shop around instead of blindly auto-renewing:

“The good news for consumers in many states is that they may be able to keep premium increases low, depending on the plan they choose,” said Elizabeth Carpenter, director at Avalere. “However, low-cost plan options in 2016 may not be from the same insurers who offered these plans in 2015. In these markets, consumers will need to balance continuity of care with lower monthly premiums when comparing their health insurance options.”

Last year around 30% of those who renewed/re-enrolled in exchange policies for 2015 did so actively...that is, they shopped around. Some kept the same plan, some switched, but they at least looked around at their options.

Hopefully, that number will increase substantially as more people grow comfortable with the idea and as technical improvements help streamline the process.

UPDATE: Thanks to farmbellpsu for the heads up re. this CNBC story by Dan Mangan which cites a different study by HealthPocket, which comes to a very different conclusion regarding average rate hikes next year:

Health insurance premiums for individual plans in major U.S. cities would rise by an average of 12 percent in 2016 if the newly proposed prices are approved, a new analysis finds.

And prices would increase even more—14 percent on average—for people enrolled in the most popular type of Obamacare plans, known as "silver" plans, the HealthPocket study reveals.

..."I was expecting somewhere between the 6 to 8 percent range," said Coleman, whose company looked at proposed rates in and around the largest cities in 45 states for a 40-year-old nonsmoker.

HealthPocket's analysis comes on the heels of the federal government releasing information about only those insurers who are asking for price increases of 10 percent or more. The company looked at rate filing requests for all insurers in the major cities, not just those who want double-digit hikes.

So...

- One study looks at Silver plans across 8 entire states and concludes the average is around a 5.8% increase request.

- Another study looks at Silver plans in 45 states...but only for the largest cities in each one...and concludes the average is around a 14% increase request.

The bottom line? 2016 Rate requests are gonna vary widely depending on the specific plan, the specific metal level, the specific network type, the specific company, the specific geographic area, the specific state, and the age of the specific person in question...

...and again, these are still just requests...and if the King v. Burwell plaintiffs win their case, all of the above is gonna be completely meaningless anyway.

Hang tight, folks.

Advertisement