RI debates exchange taxes & reveals some interesting OFF-exchange numbers

Sat, 04/11/2015 - 12:29am

On the surface, this story may seem pretty minor in the scheme of things:

Rhode Island's ACA exchange hasn't suffered from the technical glitches which are still causing problems for some states (particularly Vermont and Minnesota), but HealthSource RI does have one major problem to deal with: Funding. It's a small state with a smaller customer base for the exchange; 31,500 enrollees isn't a lot of people to cover the costs. As a result, the Governor of Rhode Island has come up with a healthcare policy tax idea which is being batted around.

The article goes into the pros and cons of the tax as opposed to simply dropping the exchange altogether and moving to Healthcare.Gov. Aside from the biggest and most obvious downside of doing so (King v. Burwell), it's also not certain that making the move would actually save any money, since HC.gov still takes some bucks to run:

Neither option is free.

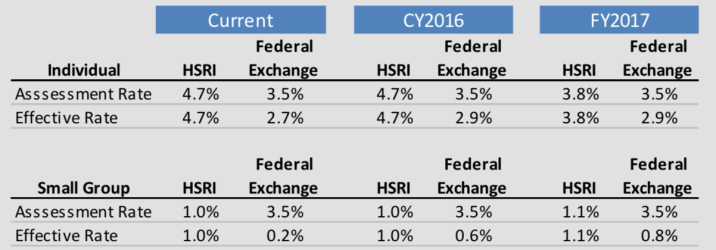

To pay for HealthCare.gov, the federal government calculates a 3.5% “user fee” on all health plans sold on the exchange – but then spreads the cost of the assessment across all similar health plans, including those sold off the exchange, which reduces the amount of the charge on each one.

To pay for HealthSource RI, Article 28 of Raimondo’s budget proposes charging two different assessment rates starting Jan. 1: a 4.7% assessment on all individual health plans sold in Rhode Island, and a 1% assessment on all small-group health plans sold in the state. That generates more money than the HealthCare.gov assessment would.

Here's the thing which captured my interest in this story, however: Note that the 3.5% HC.gov fee is spread across all "similar" policies, even those sold off-exchange.

Why is this important? Because that fact may help in calculating the elusive "Off-Exchange" QHP figure...at least for Rhode Island, anyway.

According to a chart in the article which compares the "official" and "effective" tax rates over 3 years depending on whether RI keeps their own exchange or makes the move to HC.gov, in 2015 the "effective" rate for RI at HC.gov would only be 2.7% vs. 3.5%:

In other words, if I'm reading this correctly, off-exchange QHP enrollments in Rhode Island would siphon off enough of the 3.5% fee to mean that exchange-based enrollees would only pay a 2.7% tax. How many off-exchange QHPs would this mean?

Well, the official 2015 HealthSource RI QHP enrollment as of 2/23/15 was 31,513 (out of 33,000 total plans selected).

If an equal 31.5K people enrolled in QHPs off-exchange, that would cut the exchange rate in half, from 3.5% to 1.75%. Obviously it's not 50/50.

Basic algebra should provide a rough answer, however: it looks like that 31.5K should represent roughly 77% (2.7 / 3.5) of the total QHPs sold in Rhode Island this year. That means that the other 23% are off-exchange...or roughly 9,400 off-exchange QHPs in Rhode Island.

This is a pretty tiny number, but it's useful for my purposes.

It's also noteworthy that those who compiled the table above seem to think that the ACA exchange (in RI, at least) will indeed take over a larger portion of the total individual/family healthcare policy market, increasing from 77% to around 83% over the next couple of years (2.9 / 3.5).

It's also noteworthy that on the SHOP (small business) side, this table assumes that only about (0.2 / 3.5) 6% of small business enrollments are via the RI exchange this year, but that this will increase to around 23% by 2017.

Since HSRI is reporting around 3,300 lives covered by exchange-based SHOP policies at the moment, that suggests that off-exchange SHOP enrollments are roughly 55,000 state-wide, assuming I'm understanding the table correctly.

Advertisement