Paid/Unpaid? 1/3 of all QHP coverage won't even start until AFTER March 31st!

Fri, 03/14/2014 - 10:23am

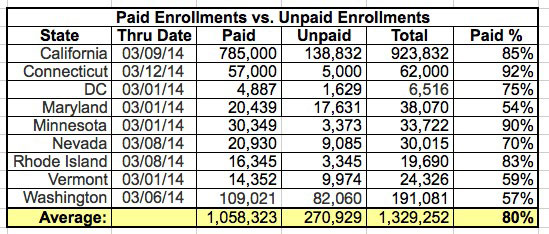

UPDATE: CNBC Reports that 2 additional states (well, one state, Minnesota, as well as DC, anyway) have released their paid/unpaid data; the chart has been updated below, which changes...nothing really; Minnesota is at 90% while DC is at 75%, and Vermont's paid rate has apparently fallen from 85 to 59%...between the three they seem to have cancelled each other out.

I've written about the "But How Many Have PAID???" issue many times before, but going into the final stretch, I wanted to explain my reasoning as clearly as possible.

The following chart only includes states which have broken out Paid vs. Unpaid Enrollments. If you only use these 9 states as a guideline, it looks like the paid rate is around 80%:

However, note that there's a growing concensus that the overall "paid" average is closer to 85%, not 80. The following is from an article about California's exchange from March 9th:

The numbers of nonpayers varied only slightly among the largest insurers on the exchange: Kaiser Permanente reported that 13 percent of its enrollees didn't pay. Anthem Blue Cross of California, Blue Shield and Health Net said it was closer to 15 percent.

Federal officials say they've noticed the same trend nationwide.

While the article above only refers to enrollments through January 31st, a follow-up press release from CoveredCA itself on March 13 states that 85% of all enrollees (through March 9th) have paid up:

The surge continues this month, with total enrollment in Covered California health insurance plans reaching 923,832 through March 9.

...Lee said insurance companies are reporting that 85 percent of all enrollees have paid their first month’s premium.

Considering that California represents nearly 21% of all QHP enrollments to date nationally, until I receive solid data otherwise, I'm going to stick with 85% paid.

There's two more factors to consider as well, however:

- First, this is a rolling average. People who enrolled between 2/16 and 3/15 don't even start coverage until April 1st, while anyone who enrolls between 3/16 - 3/31 won't start coverage until May 1st. In many cases, their first month's premium won't even be due until up to 6 weeks or more after they enroll. Considering how many people wait until the last minute to pay their bills, it's silly to write these people off as deadbeats. The vast majority of these will eventually be paid up, it's just that we won't have confirmation of many of them until well into MAY.

Consider the following: Around 3.6 million people had enrolled in QHPs (paid + unpaid) on the exchanges as of February 15th. We'll be at a minimum of 4.5 million as of tomorrow (March 15th).

- If the 3/31 total ends up being 5.5 million, 16% of those (900K) won't have their coverage start until April 1st and another 18% of the policies (1 million) won't start until May 1st.

- If the 3/31 total ends up being 6.0 million, 15% won't start until April 1st, and a full 25% (1.5 million) won't start until May 1st.

- If the 3/31 total ends up being 6.5 million, 14% won't start until April 1st and a whopping 33% (2 million) won't start until May 1st.

So again, when the deadline hits, I'm not gonna worry about 15% of enrollments not being paid when 34% or more of the policies haven't even started yet.

- Second, there have been countless stories of the payment being made but the insurance company screwing up, due to their billing system being messed up, their notification system failing to confirm reciept and so on. My own family is an example of this--we made our payment to BCBSM back in December via auto-pay right after we enrolled for January coverage...but BCBSM's system messed up, sent us three sets of cards (they had to cancel 2 of them), and didn't actually confirm our December payment for January coverage until early February. I've heard numerous similar tales, where the payment problem was not the fault of the customer or the exchange itself, but the insurance company. Here's a similar story from one of the articles linked to above:

For some Californians, however, the biggest problem wasn't paying for a plan, it was getting confirmation that their payment had been processed.

It took Woodside resident Jennifer Jones and her husband a nerve-racking seven weeks and two payments -- the first paid by check, the second online -- before their insurance company finally acknowledged that they were insured.

"It was extremely chaotic, just a nightmare," said Jones, a marketing consultant, who stopped payment on the initial check she wrote after waiting seven weeks for the insurer to cash it.

I have no idea how many people fall into this second category, but it's certainly more than a handful.

As a result of both of the above, I'm assuming roughly 1/3 of that 15% "unpaid" shouldn't really count as such, and in fact think I'm being pretty conservative in this estimate.

Thus, on the spreadsheet and graph I have the bare minimum QHP enrollment number as 90% "paid or unpaid for legitimate reasons" (and I suspect the actual % who do end up paying will be much higher...but we won't know that until sometime in May).

Now, certainly the "deadbeat" issue is still cause for some amount of concern, as are the remaining data transfer issues that some of the exchange websites are still having. The non-payment percentag probably will end up being higher for exchange QHPs than the industry norm, and if the exchanges are still screwing up with their data transfers to the insurers, that's definitely a problem. However, it's also not as simple as just "lopping off 15%" from the total for "non-payment" either.

Frankly, I'm willing to bet that when the dust all settles by late May, the actual PAID enrollments will be a good 95% of the total. I'm sure the non-payment rate will be higher than the typical industry average (which I assume is 1-2% or so? Just a guess), but it doesn't sound like a catastrophe either.

Advertisement