California: Trump sabotage could = up to 49% hikes, 340K losing coverage

Fri, 04/28/2017 - 4:59pm

Here's yesterday's press release from Covered California referred to by Dan Mangan of CNBC a little while ago:

New Analysis Shows Potentially Significant Health Care Premium Increases and Drops in Coverage If Federal Policies Change

- California’s premiums could rise by 28 to 49 percent in 2018, and up to 340,000 consumers could lose individual market coverage if changes are made to existing federal policies.

- The potential rate increase would mean billions of dollars in additional federal spending. The 1.2 million consumers who do not receive subsidies would bear the entire brunt of these increases.

- The potential decrease of 340,000 insured consumers would not only represent many individuals losing access to potentially life-saving care, but it would result in a sicker risk mix in the individual market and higher premiums for everyone.

SACRAMENTO, Calif. — A new analysis shows the dramatic consequences facing Californians if federal policies are changed from the current structure and there is no longer direct federal funding of cost-sharing reduction (CSR) reimbursements and the individual shared responsibility payment is not enforced when a consumer chooses not to purchase coverage.

The analysis found that Covered California health plan premiums could rise up to 49 percent if two key elements that have been in place for the past four years are changed: Cost-sharing reduction reimbursements are no longer directly funded as reimbursements to carriers, and the shared individual responsibility payment is not enforced.

Everything above is stuff I've been warning about/writing about for months. However, there's some other handy data nuggests in the press release and analysis which are also pretty helpful for purposes of this website:

The high potential rate increases would lead to hundreds of thousands of subsidized individuals deciding to go without insurance. For those who decide to keep their coverage, they would likely face relatively little impact, since their federal subsidies would also increase. The 1.2 million Californians on the individual market who do not receive subsidies, both in Covered California and off exchange, would pay the full cost of any premium increases. The full analysis can be found here.

When you click through to the PriceWaterhouseCoopers analysis, here's the relevant part:

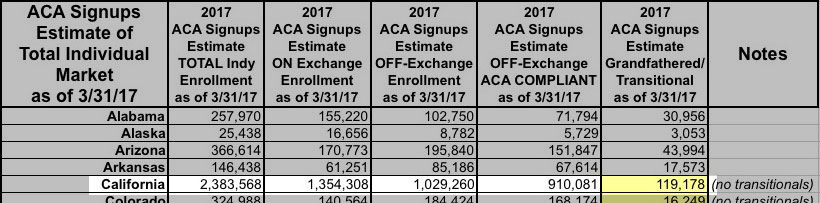

Millions Affected by Uncertainty: There is great uncertainty about the federal policies that have been in place for the past four years and are critical to the stability of the nation’s health care markets. Health plans across the country are making business decisions for 2018 that will affect the coverage of approximately 19 million Americans who get their insurance through these nongroup markets. California has about 2.4 million individuals in this market, with 1.3 million getting their insurance through Covered California and 1.1 million purchasing directly from insurers “off exchange.”2

Then, looking at the footnotes:

Using the most recent publicly available administrative data (December 2015), we estimate that 800,000 off-exchange consumers are in Affordable Care Act-compliant plans and the remaining 300,000 are enrolled in grandfathered plans that are not available for purchase.

Boom. Let's see how this compares with my own CA indy market breakout estimates from a couple of weeks ago:

Hmmmm...well, I got the first three numbers pretty much dead on:

- 2.38 million total (vs. 2.4 million actual via PWC)

- 1.35 million exchange-based (vs. 1.3 million actual via PWC)

- 1.03 million off-exchange (vs. 1.1 million via PWC)

However, it looks like my estimates of the off-exchange breakout are off quite a bit for California:

- 910K ACA-compliant (vs. 800K actual via PWC)

- 119K Grandfathered (vs. 300K actual via PWC)

In other words, while I estimated grandfathered/transitional (GR/TR) plans at only around 10% of the total indy market, in CA it appears to be around 12.5%.

Nationally, this suggests that off-exchange ACA compliant enrollments are a bit lower than I thought while grandfathered/transitional plans are somewhat higher. This ranges a lot from state to state, however; for instance, in Florida grandfathered and transitional plans combined made up 35% of the total market in August 2014...but had plummeted to just 13.2% of the total just 7 months later (March 2015). Seeing how another 2 years have passed since then, it's safe to assume that these numbers are substantially lower by now. More to the point, PWC also puts the total indy market at around 19 million vs. the 17.7 million estimated by Mark Farrah Associates and myself, so there's a lot of wiggle room here.

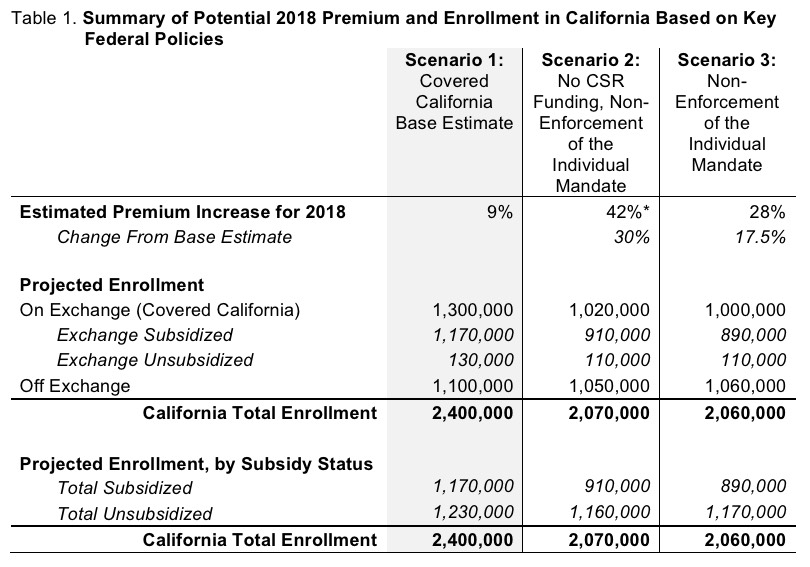

The CoveredCA PWC analysis mainly focuses on rate hikes and enrollment projections based on three different scenarios:

- Base estimate assuming no federal policy changes (best case)

- No direct federal funding for CSRs and non-enforcement of the individual mandate (worst case)

- Continued direct federal funding for CSRs but non-enforcement of the individual mandate (half case)

Here's all three potential scenarios projected by PWC:

Advertisement