Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

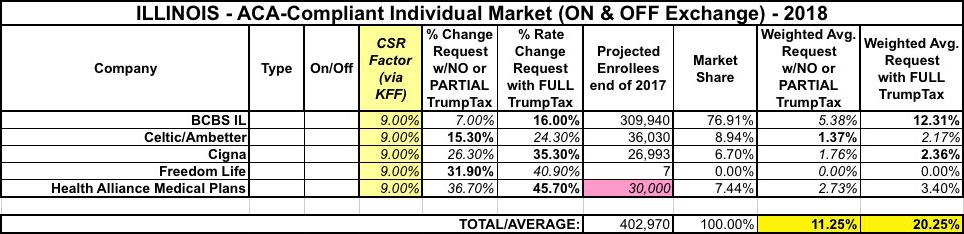

Another major state: Illinois. I've decided to scrap the "Low/High Increase" columns since they just confused people and made the table too wide, but replaced them with a new column showing the CSR factor estimate according to the Kaiser Family Foundation. Note that the percent listed will be smaller than Kaiser's estimate for each state, because their numbers only apply to silver plans, not all metal levels.

For instance in Illinois, Kaiser estimates that carriers would have to raise rates by 14% on Silver plans to cover their CSR losses. However, only 64% of Illinois exchange enrollees have silver plans to begin with, so I'm only plugging in about 9%. There are 5 carriers operating on the Illinois individual market (well, really 4, since "Freedom Life" doesn't count). I have the hard enrollment numbers for 4 of the 5; for Health Alliance Medical Plans I used 30,000 based on their 2016 number. Overall, Illinois is looking at around 11.3% w/partial sabotage, 20.3% with full sabotage:

Illinois is pretty straightforward. Assuming 400,000 people enroll in exchange policies by the end of January (a modest 3% increase over last year), I estimate around 275,000 of them would be forced off of their private policy upon an immediate-effect full ACA repeal, plus the 643,000 enrolled in Medicaid expansion as of June 2016, for a total of just over 918,000 Illinoisians kicked to the curb.

As for the individual market, my standard methodology applies:

UnitedHealth Group Inc., the biggest U.S. health insurer, is scaling back its experiment in Obamacare markets as its Harken Health Insurance Co. startup withdraws from the two exchanges where it was selling plans.

Harken will not offer individual plans through Obamacare exchanges in Georgia and Chicago in 2017, the company said Thursday in an e-mailed statement. It will continue to offer individual plans off the exchange, Harken said.

As commenter ME notes, there are currently around 22,800 Harken enrollees in Illinois and another 10,500 in Georgia. I have no idea what the on/off exchange ratio is, however, so the number of people who will actually have to shop around will be up to 33,300; assuming, say, 2/3 are on the exchange, that would be roughly 22,000 people.

An important reminder from an anonymous tipster for any Illinois resident who was enrolled in a policy via the now-defunct "Land of Lincoln" Co-Op:

Hey hey. Just wanted to pass some info to you in case you can get it out there. As of last week (not sure the date - either the 15th or the week after) only 34% of LOLH members had taken advantage of the SEP. Spoke with legislators yesterday to get the word out, but since the deadline is Friday, we are trying to get the word out for people to get enrolled.

Usually when state regulators publicize their approved rate changes for carriers on the independent market, they list the various carriers and the approved average rate changes for each. I then simply plug these into my existing spreadsheet and get a before/after comparison against how much the carriers actually requested.

In the case of illinois, it's a little trickier. Unless I'm missing something, the only official notice the IL DOI has released is this PDF, which--while including lots of useful info about rating areas and so forth--doesn't actually list the overall statewide average approved rate increases by carrier.

Instead, it lists the averages based on metal level, and even then doesn't list all of the plans, just selected ones: Lowest-price Bronze, Lowest and 2nd Lowest-price Silver, and Lowest-price Gold, like so:

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

(Note: I've had to re-work some of this entry thanks to clarifications from Adam Cancryn about the RBC rule; too many little edits to document each one).

Last week I posted about the latest ugly Co-Op meltdown, this time Land of Lincoln Health (LoL) of Illinois.

As pointed out in my follow-up entry, given the precarious financial state LoL was already in last year, it made little sense that they only asked for fairly nominal rate hikes:

Now, since LoL went belly-up mid-year regardless, obviously even those massive rate hikes weren't enough to save them, so the question is, what would have happened if LoL had gotten their nominal increases as requested?

The most recent ACA/healthcare news out of Illinois was the ugly announcement that Land of Lincoln Health is the latest ACA-created Co-Op to go belly-up, leaving 49,000 people (39,000 on individual plans and 10,000 in the small group market) having to scramble to find new coverage in the middle of the year. This was on top of recent news that UnitedHealthcare is pulling out of dozens of states including Illinois (Humana is also dropping out of a bunch of states, but I don't think Illinois is among them).

Well, nature (and the market) abhors a vacuum, so guess what?

One of the nation's largest health insurance companies plans to enter the Obamacare marketplace in the Chicago area for the first time, bringing new competition as other insurers exit or go out of business.

Likely stupid question here, but if they were doing this bad financially that they couldn't even make it though all of 2016, then how come when requesting their 2016 rates last year they (apparently) asked for less than a 10% bump?