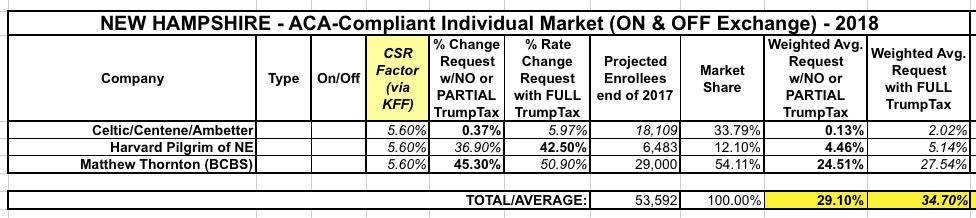

As noted earlier today, I've now managed to plug 48 states (plus DC) into my 2018 Rate Hike Project spreadsheet. This leaves just two states missing: New Hampshire and Texas. I'm still waiting to clarify some things for each, so this analysis could still change, but I really want to wrap this up, so here's what I have for New Hampshire right now:

When I first ran the numbers for New Hampshire'srequested 2018 rate increases, it seemed pretty straightforward: 3 carriers on the individual market. 2 listed rate changes assuming CSRs would be paid; one assumed they wouldn't. This gave the following:

With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

I'm still missing final 2018 rate data for 6 states, but in the meantime I'm also doing some cleanup of some of the states I thought I already had final data for. Today both my home state of Michigan as well as Washington State released their official, approved increase tables.

However, I do give the Michigan Dept. of Insurance & Financial Services huge credit for making it incredibly easy for me to plug their data in. Look at that...they list all carriers, whether they sell on or off exchange, the exact average rate increases, and even include the number of affected enrollees, which is usually the hardest number for me to track down. Thanks, MI DIFS!!

Still, I don't like loose ends, and those 8 missing states are bugging me, so I still want to fill them in for completeness' sake. The only big state remaining is Texas, but I'm also missing Alabama, Hawaii, Iowa, Missouri, New Hampshire, Oklahoma and Wyoming.

A week or two later, the ASPE department of CMS issued a report putting the average at 22%...except that they were missing 7 states, only included benchmark Silver plans and didn't include off-exchange policies. The missing states had higher average premiums on the whole, so I'm pretty sure the actual overall average was pretty close to 24-25% in the end.

When I ran the requested rate hike numbers for Kentucky in early August, it looked like the only 2 carriers participating in the individual market next year (CareSource and Anthem BCBS) were asking for pretty hefty hikes of around 30.8% on average...and that assumed CSR reimbursement payments would be made next year. If they aren't, based on the Kaiser Family Foundation's estimates, I tacked on an additional 13.8% for a requested average of 44.3%. Ouch.

Washington, D.C. – The District of Columbia Department of Insurance, Securities and Banking (DISB) approved health insurance plan rates for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2018.

Insurers filed their initial rates with the Department in May. Since then, DISB engaged in its rate review process resulting in two out of the four insurers revising their rates down from their initial filings, one as much as half of what was proposed. The Department also held a public hearing during the rate review process to allow residents to provide input in the rate review process.

Back in August, I posted a rough analysis of the requested rate increase situation for Wisconsin's individual market carriers. However, I cautioned at the time that I was missing the enrollment market share numbers for four of the carriers (Aspirus, Compcare, Wisconsin Physician Service and WPS), and therefore had to guess at how the rate hikes for those carriers would impact the statewide average. I estimated the numbers assuming CSR payments are made at 21.7%, and from that assumed the impact of CSR reimbursements not being made would be around 7.8 additional points being tacked onto the average.

A couple of weeks ago, the state insurance commissioner announced the approved rate increases. The good news is that I overestimated on the "CSRs paid" front. The bad news is that I underestimated on the "CSRs not paid" front: It's actually 20% and 36% respectively:

I've written a lot in recent weeks about the real world impact that Trump cutting off CSR reimbursement payments will have on 2018 premiums in various states depending on how they choose to load the additional cost. As I've noted repeatedly, there are basically four strategies they can take: They can assume the payments will continue; they can spread the load across all ACA-compliant policies; they can load all of the cost onto Silver plans only; or they can load all of the cost onto on-exchange Silver plans only, while also creating (if one doesn't exist) a special off-exchange-only Silver plan as a backstop for unsubsidized Silver enrollees (aka the "Silver Switcharoo").