ACA Repeal Impact

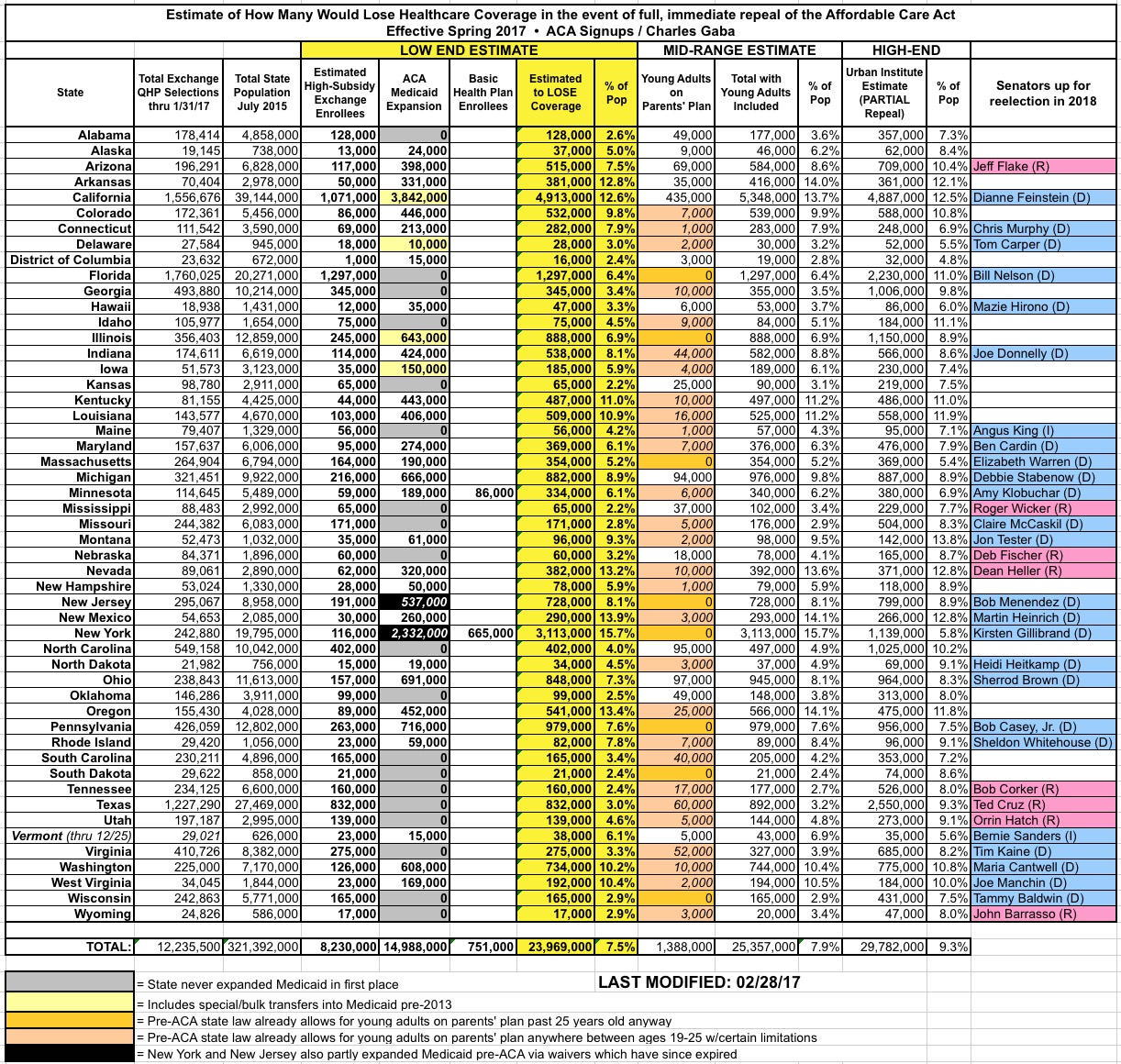

UPDATE 1/17/16: This morning the Congressional Budget Office released their projections of how many people would likely lose healthcare coverage if the GOP proceeds with a partial repeal of the Affordable Care Act. My state- and county-level estimates assume a full repeal (including wiping out regulations like guaranteed issue, community rating and so forth), which I estimate would add up to around 24 million people without including "Young Adults on Parents' Plans", or around 25.3 million with them included.

The CBO's projection, however, like the Urban Institute's, assumes a partial repeal, which would remove Medicaid expansion, federal subsidies and the individual/employer mandate penalties...but would leave the rest in place. This would actually have a more devastating impact, as it would decimate the off-exchange (full-price) individual market as well. They project around 32 million people losing coverage by 2026 under this scenario...or roughly 8 million more individual market enrollees than the 8.9 million I'm estimating under the full repeal scenario.

Of course, the number of off-exchange indy plan enrollees varies widely from state to state and even county to county, but if you want to get an idea of how the state/county-level numbers would look under the CBO "partial repeal" projection, simply double the number of individual market enrollees to each state/county.

For instance, in Oakland County, Michigan, my estimate is ~35,000 highly-subsidized exchange enrollees and ~53,000 Medicaid expansion enrollees, or around 88,000 total. Under the CBO's projection, I'd add roughly 35,000 more off-exchange and unsubsidized on-exchange enrollees, for a total of ~123,000 people losing coverage.

Alternately, you could just increase the TOTAL number for each state by around 1/3 to get a rough idea of the maximum possible devastation.

I've pulled together all of my state/county-level breakout entries into a single location (scroll down for links to individual states). This way people can look up specific states to see what the potential impact of the ACA being repealed would be in terms of people losing their healthcare coverage. I even added this link to the main menu above.

Remember: I'm only including those who I expect could lose their coverage, not the impact to Medicare, pre-ACA Medicaid, Group Coverage and so on.

Some important caveats which apply to all county-by-county breakouts, and a few which only apply to specific states:

YOUNG ADULTS ON PARENTS' PLANS:

- In the full 50-state summary, I include an extra column for "Young Adults on their Parents' Plan"; there's around 3.1 million of these folks nationally. I only estimate around 1.4 million of them are actually at risk of losing their current policy coverage because about 2/3 of the states already had a similiar law on the books at the state level prior to the ACA, though the specific provisons and cut-off ages varied. I've taken my best guess at how many wouldn't be protected by pre-existing (hah!) laws.

- In addition, I have no county-level data whatsoever for the "Young Adult" numbers. Since this is probably the most likely part of the ACA to survive any repeal/replacement anyway, I've chosen to leave this category off of the individual state tables altogether.

MEDICAID EXPANSION:

- In nearly all ACA Medicaid expansion states, these are hard numbers taken directly from the state public health department websites, quarterly/monthly reports and so on. The "as of" date varies from state to state, but all are within the past year.

- For Arizona, the county-level Medicaid data wasn't split between "traditional" and "ACA expanded", but statewide, expansion enrollees make up about 21% of the total, so I'm assuming 21% of each county's Medicaid enrollees are expansion-specific.

- Louisiana just launched ACA expansion in July, and has already signed up 374,000 people...who might be kicked right back off again.

- New York and New Jersey's ACA expansion numbers are a bit complicated: Both states had already partly expanded Medicaid before the ACA using a waiver arrangement with the federal government. Then the ACA expanded Medicaid a bit further in each state. Then the original waiver expired...but no one bothered renewing them since the ACA made it moot anyway. This means that if the ACA actually is repealed, not only would those made eligible for Medicaid in each state be kicked off, but so would everyone enrolled via the now-expired waiver.

PRIVATE PLANS VIA THE ACA EXCHANGES:

- The Centers for Medicare & Medicaid provided a handy county-level ACA exchange enrollment breakout for the 38 states which were handled by HealthCare.Gov last year. This includes the total number of people who selected Qualified Health Plans (QHPs) via HC.gov as of 2/01/16. For each county, I start with that number, then modify it via several steps:

- First, I multiply it by the projected increase (or in some cases, decrease) in total QHP selections by the end of January.

- I then take the percentage in each county expected to receive Advance Premium Tax Credits (APTC) (ie, federal subsidies), since those paying full price now are unlikely to lose their coverage (Note: I'm assuming the entire individual market won't collapse, which is also a distinct possibility)

- I then lop 10% off of that number to account for those who simply never end up paying their first month's premium to begin with, and are thus never enrolled in the first place

- Finally, I reduce that number by another 10% to remove those who are only receiving nominal subsidies, and who therefore would likely be able to suck it up and hold onto their policies.

For example: Let's suppose that in a given county, 10,000 people selected QHPs during open enrollment last year, of which 85% received subsidies, in a state where I expect about 5% growth this year.

My estimate would be: 10,000 x 1.05 x 0.85 x 0.90 x 0.90 = 7,229 people enrolled, effectuated & receiving subsidies high enough that they'd be seriously screwed if taken way.

- I've found county breakouts for some of the remaining 12 states, but not others; like the Medicaid numbers, some are elusive.

Finally, there's no need to "break out" the District of Columbia numbers; I assume the whole District is basically considered a single county.

Pages

Advertisement