Over the past week or so there was a lot of tense negotiations and confusion about whether or not ConnectiCare, the 2nd largest carrier on Connecticut's exchange and the largest in CT's individual market overall, would bail on participating on AccessHealthCT next year. They bumped up their rate hike request not once but twice, from 14.3% to 17.4% to 27.1%, and when state regulators stuck with 17.4% and refused to budge any higher, they threatened to file a lawsuit and drop out of the exchange. As of last Friday, it looked like they were indeed pulling out.

Days after declaring it would leave the state’s health insurance exchange, ConnectiCare has decided not to drop out of the marketplace, much to the relief of many — including Gov. Dannel P. Malloy.

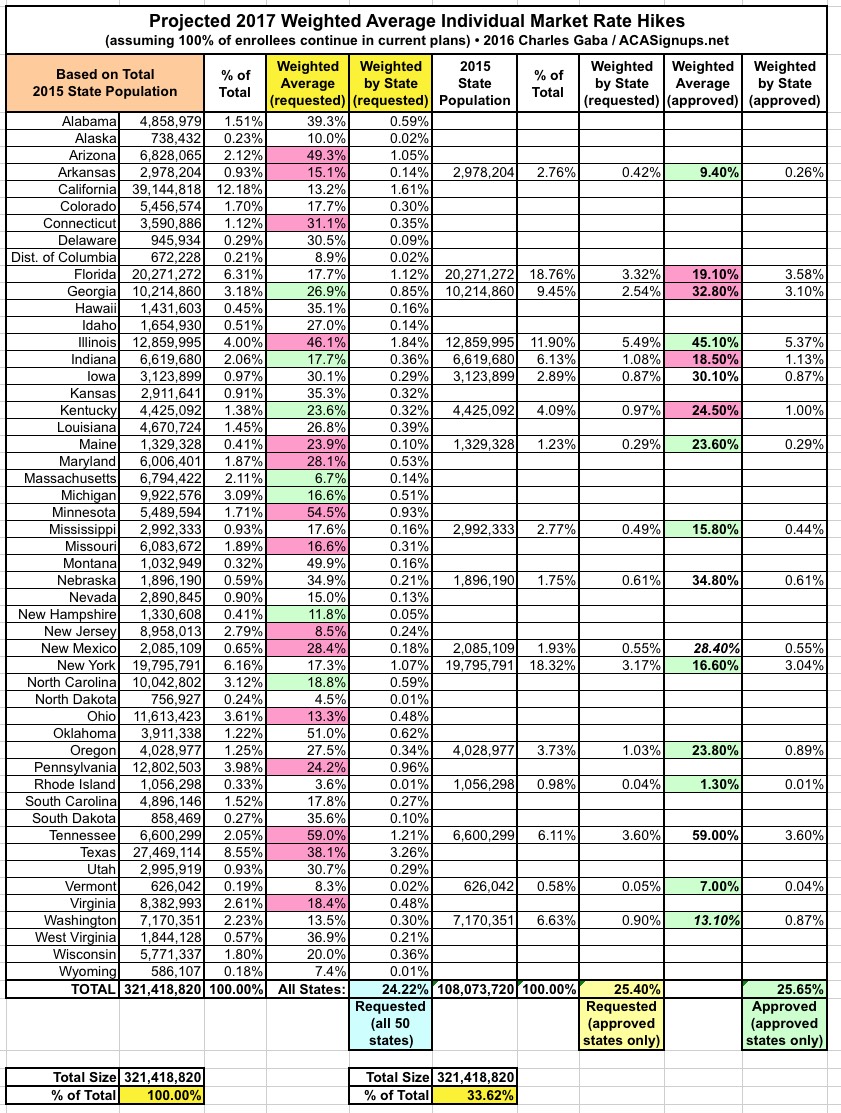

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

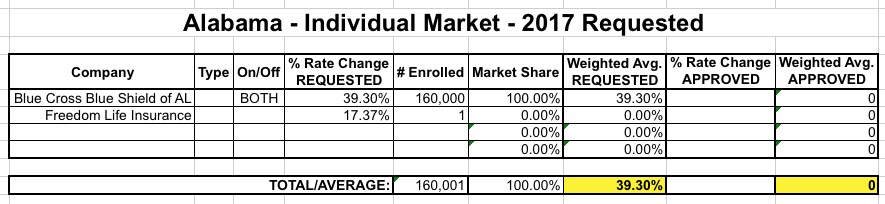

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

The cost of health insurance plans offered under the Affordable Care Act will jump 20 percent or more next year under rates to be announced Friday by Maryland regulators.

His remarks came as the Maryland Insurance Administration approved double-digit rate increases for the four companies that sell health plans through the state exchange, an online marketplace set up under the law for people who cannot buy coverage through their employer.

...CareFirst, which holds 68 percent of the market, received an average hike of 31.4 percent on its PPO plan and 23.7 percent on its HMO — the highest increases of any insurer.

...Rates in Maryland also have been typically lower than those nationally under the Affordable Care Act, so there could be some normalizing going on, said John Holahan, a fellow in the Urban Institute's Health Policy Center.

"Maryland rates have been lower than the rest of the nation so it seems some catching up should be expected," said Holahan.

When I first ran the numbers for New Mexico back in May, the average requested rate hike for the indy market appeared to be about 24.9%. Since then, however, there have been three major changes: First, Presbyterian Health Plan decided to drop off the exchange (although they'll still be around off-exchange). Second, it looks like CHRISTUS bumped up their request from 12.3% to 15.78%; and third, Molina Healthcare, which had been requesting a refreshingly modest 3.8% hike, resubmitted their request at a much higher 24% average increase.

Three of the 5 carriers had their final requests approved exactly as is by state regulators. CHRISTUS and Molina have yet to be approved, but based on a lengthy online conversation with someone very much in the know about the New Mexico health insurance market, I'm highly inclined to believe that both of their final asks will be approved as is as well.

The Washington Insurance Commissioner just issued the following press release. On the surface, it looks straightforward: 13.5% avg. requested, 13.1% approved. However, it's more complicated than that, because that 13.1% figure only applies to fewer than half of the plans (46 out of 98). The other 52 are still being reviewed:

OLYMPIA, Wash. – The Office of the Insurance Commissioner (OIC) has approved 46 individual health plans from seven insurers who will offer them in the Exchange, Wahealthplanfinder (www.wahealthplanfinder.org), for sale in 2017. The Washington Health Benefit Exchange Board is scheduled to certify the approved insurers and their plans at its board meeting later today.

Regence Blueshield also filed 21 plans for sale in the Exchange and Bridgespan filed 31 plans. Both companies’ filings and rates are still under review. They must be approved by the OIC before they can be considered for certification by the Exchange.

Arizona’s Pinal County Gains Health-Law Exchange Insurer

Blue Cross Blue Shield of Arizona will offer plans on the Affordable Care Act exchange in Arizona’s Pinal County next year, resolving a situation that drew a national spotlight because it represented a major challenge to the mechanics of the health law.

When Aetna Inc. announced last month that it would withdraw from the exchange in Arizona, among other states, it left Pinal at risk of becoming the first U.S. county without a single insurer selling exchange plans. Aetna had been expected to sell exchange plans in Pinal County, where approximately 10,000 people had signed up for ACA plans.

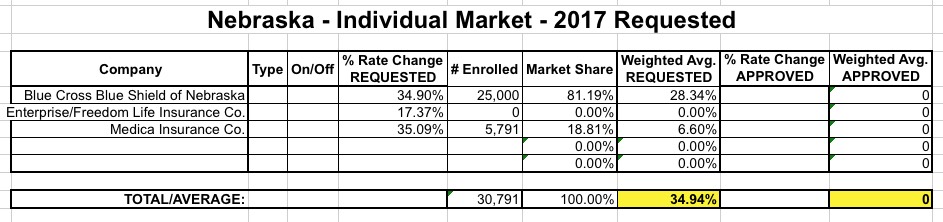

Huh. Back in June, when I first ran the requested rate hike numbers for Nebraska, it looked as though there were only two real carriers offering individual plans, either on or off the exchange: Blue Cross Blue Shield and Medica. UnitedHealthcare announced they were leaving NE along with a bunch of other states, and Coventry (aka Aetna) didn't have any filings for 2017, so I assumed they were bailing as well. Finally, the less time spent talking about "Enterprise/Freedom Life" the better. So...it looked like BCBS and Medica were it. Here's what the table looked like:

The Connecticut average requested rate hike has jumped around a lot over the summer. It started out at roughly 21.3% back in June, then increased to 22.2% after the HealthyCT Co-Op announced they were closing up shop. Then, several of the carriers submitted revised rate hike requests, bumping the average up further to around 26.8%.

Well, over the holiday weekend, the CT Mirror reports that the CT Dept. of Insurance released their response to the requests. There were also yet more last-minute filing changes. I've updated the spreadsheet with both the final requests as well as the approvals...but there are a copule of major blank spaces I still have to fill in:

Most Connecticut health insurance plans sold through individual and small group markets will undergo steep rate hikes next year, although in some cases, the prices will not go up by as much as carriers had sought.

When I last crunched the numbers for the 2017 individual market in Arizona, the average requested rate hike statewide was a whopping 68%. However, that was before Aetna dropped their bombshell about dropping out of the exchanges in 11 states (AZ included), leaving about 6,400 residents receiving ACA tax credits in Pinal County with no subsidized policy options whatsoever.

Since Aetna had intended on requesting a jaw-dropping 85.8% average rate hike if they had stuck around, this technically meant that the average requested hike for the other carriers would have dropped somewhat, although this would be limited by Aetna only having about 7% of the individual market in the state.