Arise Health Plan, a subsidiary of WPS Health Solutions, said Thursday that it will not sell health plans on the marketplaces set up through the Affordable Care Act next year, becoming the latest company to abandon the market.

Arise and WPS Health Insurance also will sell only high-deductible health plans for individuals and their families off the marketplace, and those plans will be available only in a limited number of counties.

...For now, the marketplace for Milwaukee County next year will have four companies offering health plans: Molina Healthcare; Network Health Plan, owned by Ascension Wisconsin and Froedtert Health; Common Ground Healthcare Cooperative; and Children’s Community Health Plan.

Waukesha County tentatively will have those companies as well as Anthem Blue Cross and Blue Shield in Wisconsin and Dean Health Plan.

...Arise Health Plan has a relatively small share of the market in southeastern Wisconsin.

There's been story after story over the past few months about insurance carriers large and small either dropping out of the ACA exchanges or (in the case of 4 co-ops) going belly-up altogether. Along the way, there have also been a few stories about other carriers expanding into new states or additional counties in states they're already participating in.

Residents in more West Virginia counties will have additional health plan options when the open enrollment period on the Mountain State’s insurance exchange, created in the Affordable Care Act, opens on Nov. 1.

In its 2nd year in West Virginia, CareSource, a nonprofit managed care provider based in Dayton, Ohio, is expanding its coverage area to include 32 counties.

...In 2016, CareSource is providing health insurance coverage to more than 1,300 West Virginia residents in ten counties: Brooke, Cabell, Hancock, Kanawha, Lincoln, Marshall, Mason, Ohio, Putnam, Wayne.

Two bits of news out of the DC exchange today: First, they announced that the uninsured rate has been slashed in half over the past 3 years thanks in no small part to the Affordable Care Act. Not a huge shocker given the recent surveys/studies released by the CDC, Gallup, Kaiser and so on of late, but still good to see:

Washington, DC – A new survey by the Center for the Study of Services conducted for the DC Health Benefit Exchange Authority (DCHBX) concludes that the District of Columbia made huge gains during the most recent open enrollment period to provide access to health insurance coverage to people who were previously uninsured. Results from this survey show that more than 25,500 people, who were not previously covered in 2015, gained access to health insurance coverage in 2016 through DC Health Link, the District’s online health insurance marketplace.

UnitedHealth Group Inc., the biggest U.S. health insurer, is scaling back its experiment in Obamacare markets as its Harken Health Insurance Co. startup withdraws from the two exchanges where it was selling plans.

Harken will not offer individual plans through Obamacare exchanges in Georgia and Chicago in 2017, the company said Thursday in an e-mailed statement. It will continue to offer individual plans off the exchange, Harken said.

As commenter ME notes, there are currently around 22,800 Harken enrollees in Illinois and another 10,500 in Georgia. I have no idea what the on/off exchange ratio is, however, so the number of people who will actually have to shop around will be up to 33,300; assuming, say, 2/3 are on the exchange, that would be roughly 22,000 people.

Normally I post screenshots from the revised/updated SERFF filings and/or updates at RateReview.HealthCare.Gov, but it takes forever and I think I've more than established my credibility on this sort of thing, so forgive me for not doing so here. Besides, #OE4 is approaching so rapidly now that this entire project will become moot soon enough, as people start actually shopping around and finding out just what their premium changes will be for 2017.

The other reason I'm not too concerned about documenting the latest batch of updates/additional data is because in the end none of it is making much of a difference to the larger national average anyway; no matter how the individual carrier rates jump around in various states, the overall, national weighted average still seems to hover right around the 25% level.

Still, for the record, here's the latest...in four states (Iowa, Indiana, Maine & Tennessee) I've just updated the requested and/or approved average increases. In the other four (Massachusetts, Montana, North & South Dakota) I've added the approved rate hikes as well.

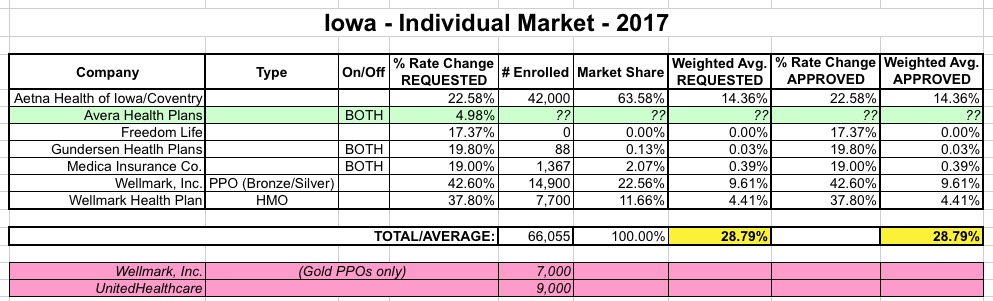

Wellmark Blue Cross and Blue Shield announced Tuesday that it will narrow its choices for individual Affordable Care Act plans in Iowa and will eliminate ACA individual plans in South Dakota altogether in 2017.

First, some clarification: Wellmark isn't on the exchange to begin with, and wasn't planning on joining it in SD next year, so this is a rare case of a carrier dropping their off-exchange individual market offerings. Since all of Wellmark's indy enrollees in South Dakota are paying full price, this one can't be blamed on APTC enrollees being sicker than average, etc.

As for Iowa, it's more of a mixed bag...Wellmark is basically swapping out higher end PPO plans for lower end HMO, which is pretty much the trend everywhere:

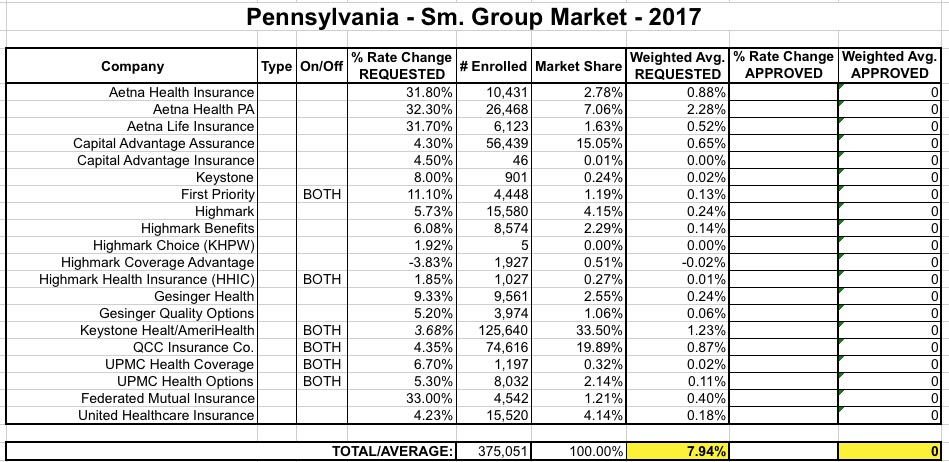

Yesterday I hobbled together the weighted average rate hikes (either requested or approved) for the ACA-compliant small group markets across 15 states. In 4 of these states, I hadn't yet tallied the weighted average, so I temporarily used the median increase for each. In the case of Pennsylvania, the range was from a 3.8% decrease to a 33% increase, with a midpoint of around 14.6%.

Today, however, I've actually plugged in the enrollment numbers for each sm. group carrier in Pennsylvania based on their 2017 rate request filings, and have come up with a weighted average of just 7.9%:

(sigh) I thought that last Friday was the deadline for carriers to decide whether they were in or out of the exchange for 2017, but between today's news out of Tennessee and now this, apparently that deadline only applies to those who will be participating in the 4th Open Enrollment Period:

IU Health Plans said Monday afternoon it had “restructured its product offerings for 2017” and no longer will be offering individual plans on the exchange. It said the change was necessary “to adapt to new market dynamics” as well as uncertainty created by withdrawals of several other insurers.

Things are looking pretty good for the ACA exchanges in states like Rhode Island, North Dakota and Massachusetts, where they're looking at single-digit rate hikes next year. However, they're looking pretty dire in states like Arizona, Montana and Oklahoma, where the average hikes are likely to be around 50% or higher for many people.

UPDATE 10/26/16: In light of yesterday's official confirmation by the HHS Dept. that my estimate of ~25% weighted avg unsubsidized rate hikes on the individual market was dead-on target, I thought it was important to pin this entry to the front of the website again.

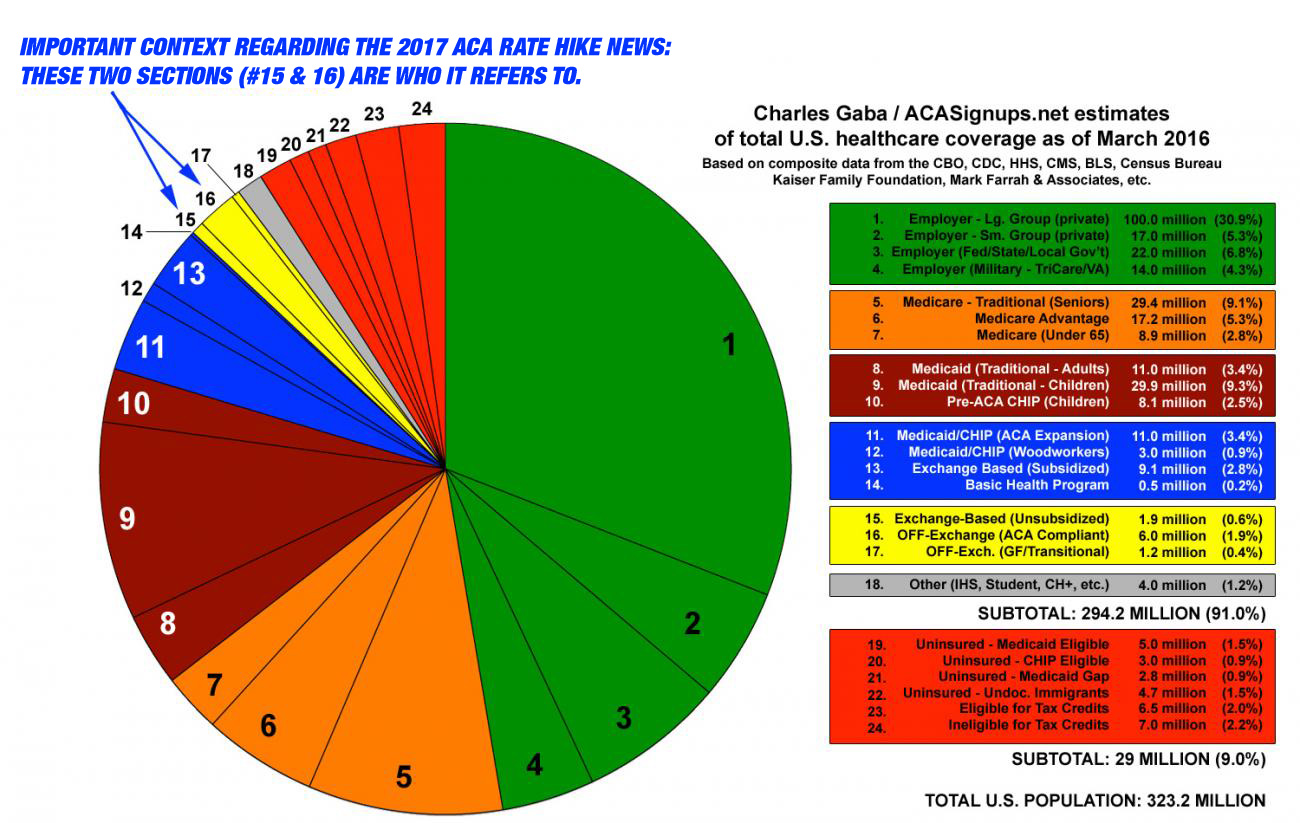

Remember that big pie chart I posted last March which broke out the entire U.S. population by type of healthcare coverage? Well, here's a modified version, showing which people will and won't be impacted by the "25% average" figure being argued about today:

A few people have asked whether or not the "25% average hikes" I've estimated which have been cited by pretty much every outlet under the sun also apply to job-based coverage.

NO! Absolutely not!

That 25% weighted national average only applies to the roughly 18 million people enrolled in ACA-compliant individual policies...and even then, roughly half of those folks are mostly protected from the hikes thanks to the federal tax credits. So we're really talking about roughly 9 million people who have to pay the full 25% average increases.