TRUTH OR CONSEQUENCES – Gov. Michelle Lujan Grisham today signed into law legislation that builds on the administration’s work to make healthcare more affordable and accessible for every New Mexican.

“Delivering quality healthcare to New Mexico’s population requires a tailored approach that takes into account rural communities, New Mexicans benefiting from Medicaid, and the tens of thousands of public employees in our state,” said Gov. Lujan Grisham. “These are bills that are going to positively impact a vast swath of New Mexicans.”

The governor signed these important healthcare bills during a ceremony at Sierra Vista Hospital in Truth or Consequences.

As an aside, I was a bit confused about the name of the city so I looked it up. Huh.

New York's implementation of the ACA's Basic Health Plan provision (Section 1331 of the law) is called the Essential Plan. It currently serves 1.2 million New Yorkers, or over 4x as many residents as ACA exchange plans do.

Under the ACA, most states have expanded Medicaid to people with income up to 138 percent of the poverty level. But people with incomes very close to the Medicaid eligibility cutoff frequently experience changes in income that result in switching from Medicaid to ACA’s qualified health plans (QHPs) and back. This “churning” creates fluctuating healthcare costs and premiums, and increased administrative work for the insureds, the QHP carriers and Medicaid programs.

It's been a whopping nine months since the last time I wrote anything about the seemingly never-ending Braidwood v. Becerra lawsuit which threatens to not only end many of the ACA's zero-cost preventative services, but which could also throw all sorts of regulatory authority into turmoil depending on what precedents it sets.

On March 30, 2023, a federal district court judge issued a sweeping ruling, enjoining the government from enforcing Affordable Care Act (ACA) requirements that health plans cover and waive cost-sharing for high-value preventive services. This decision, which wipes out the guarantee of benefits that Americans have taken for granted for 13 years, now takes immediate effect.

Enrollment Remains Open Across All Marketplace Programs for Duration of Public Health Emergency Unwind

Albany, N.Y. (February 28, 2024) – Representatives from NY State of Health, the state’s official health plan Marketplace, will make an appearance at job fairs across the State beginning next month to inform New Yorkers about their options for quality, affordable health insurance. Certified enrollment assistants will be available to help uninsured job seekers find a plan that fits their budget and health needs and guide existing enrollees through the new renewal process to keep their coverage current.

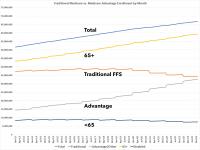

Every month for years now, the Centers for Medicare & Medicare Services (CMS) has published a monthly press release with a breakout of total Medicare, Medicaid & CHIP enrollment; the most recent one was posted in late February, and ran through November 2022.

In November 2023, 85,815,827 individuals were enrolled in Medicaid and CHIP, a decrease of 1,503,283 individuals (1.7%) from October 2023.

78,710,401 individuals were enrolled in Medicaid in November 2023, a decrease of 1,523,107 individuals (1.9%) from October 2023.

7,105,426 individuals were enrolled in CHIP in November 2023, an increase of 19,824 individuals (0.3%) from October 2023.

As of November 2023, enrollment in Medicaid and CHIP has decreased by 8,034,913 individuals (8.6%) since March 2023, the final month of the Medicaid continuous enrollment condition under the Families First Coronavirus Response Act (FFCRA) and amended by the Consolidated Appropriations Act, 2023.

Medicaid enrollment has decreased by 8,007,036 individuals (9.2%).

CHIP enrollment has decreased by 27,877 individuals (0.4%).

Between February 2020 and March 2023, enrollment in Medicaid and CHIP increased by 22,975,671 individuals (32.4%) to 93,850,740.

Medicaid enrollment increased by 22,637,644 individuals (35.3%).

CHIP enrollment increased by 338,027 individuals (5.0%).

Normally, states will review (or "redetermine") whether people enrolled in Medicaid or the CHIP program are still eligible to be covered by it on a monthly (or in some cases, quarterly, I believe) basis.

However, the federal Families First Coronavirus Response Act (FFCRA), passed by Congress at the start of the COVID-19 pandemic in March 2020, included a provision requiring state Medicaid programs to keep people enrolled through the end of the Public Health Emergency (PHE). In return, states received higher federal funding to the tune of billions of dollars.

As a result, there are tens of millions of Medicaid/CHIP enrollees who didn't have their eligibility status redetermined for as long as three years.

I strongly suspect that at least one of the remaining holdout states will join the expansion crowd this year, most likely Georgia, Mississippi or Alabama...but it likely will be some state-specific variant as described above. Stay tuned...

...As I noted, however, in all three [states] it's pretty likely they'll go with at least a partially privatized version as Arkansas has instead of a "clean" expansion of Medicaid proper.

Of course, as one Alabama-based advocate put it...

“Our partners provide a crucial one-on-one service to help Coloradans get covered,” said Connect for Health Colorado’s Chief Executive Officer, Kevin Patterson. “They help us make sure local communities, especially those who face barriers in getting health coverage, can access the plans and savings we offer. I encourage interested organizations and current partners to apply.”

HARTFORD, Conn. (Feb. 20, 2024) — Access Health CT (AHCT) today announced it will host two free, in-person enrollment fairs in February and March to help HUSKY Health enrollees who have been affected by the Medicaid Unwinding process. The events will take place in New Britain and Stamford.

Medicaid Unwinding is the process of resuming the review of households for Medicaid eligibility after a three-year break during the Public Health Emergency. The eligibility redetermination process resumed April 1, 2023 and HUSKY Health clients will be notified when it is their turn to enroll. The process will end March 31. HUSKY Health is Connecticut’s Medicaid program.

Connecticut residents who remain eligible for HUSKY Health will likely be automatically reenrolled. Those who need to take action will receive mail with instructions.