New Jersey is an important state to watch, as they (along with DC) are the first state to specifically reinstate the ACA individual mandate penalty at the exact same levels as the just-zeroed out federal version. Massachusetts has a mandate penalty in place this year as well, but a) theirs pre-dated the ACA and was simply dusted off again and b) theirs uses a different formula anyway.

Last year, Individual Market insurance carriers in New Jersey announced that average unsubsidized 2019 premiums would be reduced by an average of 9.3% statewide due to two laws put into place by the state legislature and Governor Murphy: Reinstatement of the mandate penalty at federal levels (which lowered rates by 6.8 percentage points from +12.6% to just +5.8%) and the initiation of a solid reinsurance waiver program (which reduced rates by a further 15.1 points, for a final average change of -9.3%).

Unfortunately, North Dakota is another state where the carriers have redacted their rate filings. I was able to garner some info about one of the three carriers participating in the Individual Market next year: Medica's filing redaction wasn't done properly, so I was able to extract that they're looking at medical trend of 7.7%, a morbidity reduction of 1.5%, a 2.3% increase due to the reinstatement of the ACA's insurer fee...and a 20% reduction due to the implementation of the state's reinsurance program, which I first reported on last fall and followed up with this spring.

(sigh) I'm into the home stretch with only a handful of states left to go. Unfortunately, South Carolina is yet another state where the actual enrollment numbers are either missing or redacted, making it impossible to run a properly weighted average...but again, the range between the three carriers offering individual market policies is so narrow that it doesn't make much difference anyway (between -3.72% and +0.17%).

The unweighted average is a 1.9% reduction in unsubsidized premiums statewide.

On the small group market, however, average 2020 premiums are jumping by double digits: 11.1%.

David Balat is the director of the Right on Healthcare initiative at the Texas Public Policy Foundation, a conservative think tank which pushes school vouchers and which attempts--against all sanity--to claim there's a moral case in favor of fossil fuels, which I guess should be described as "natural gaslighting."

Anyway, the other day, Mr. Balat posted an op-ed at The Hill in which he tries to gaslight America regarding the lengthy list of ACA sabotage efforts which have been (and which continue to be) pushed by the Trump Administration, some more successfully than others.

Repeated claims of sabotage of the ACA by the Trump Administration fall flat because of these important initiatives put in place by the president. Although the president has chosen to not defend the ACA in the Texas v. Azar case, he has made numerous strides to make available options to help Americans who require coverage suited to their needs, as well as help for those with chronic conditions.

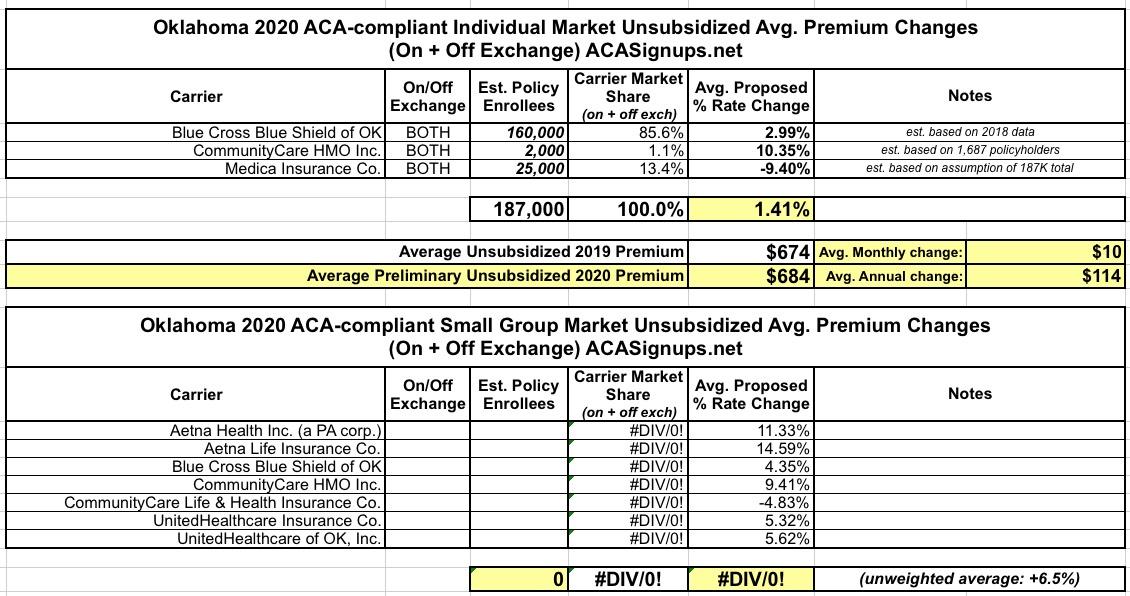

Oklahoma has three carriers on the Individual Market these days. Once again, all three rate filing memos are redacted, but I was able to dig up the number of current policy holders for one of them (CommunityCare HMO).

I've bumped that number up a bit to account for the total number of covered lives to an even 2,000. For the other two carriers, I'm assuming Blue Cross Blue Shield still holds the lion's share of enrollees and that the total on+off-exchange market is around 187,000 people.

If this is all correct, the weighted average rate increase for unsubsidized enrollees is around 1.4% statewide.

Meanwhile, the unweighted average rate hike for the small group market is 6.5%.

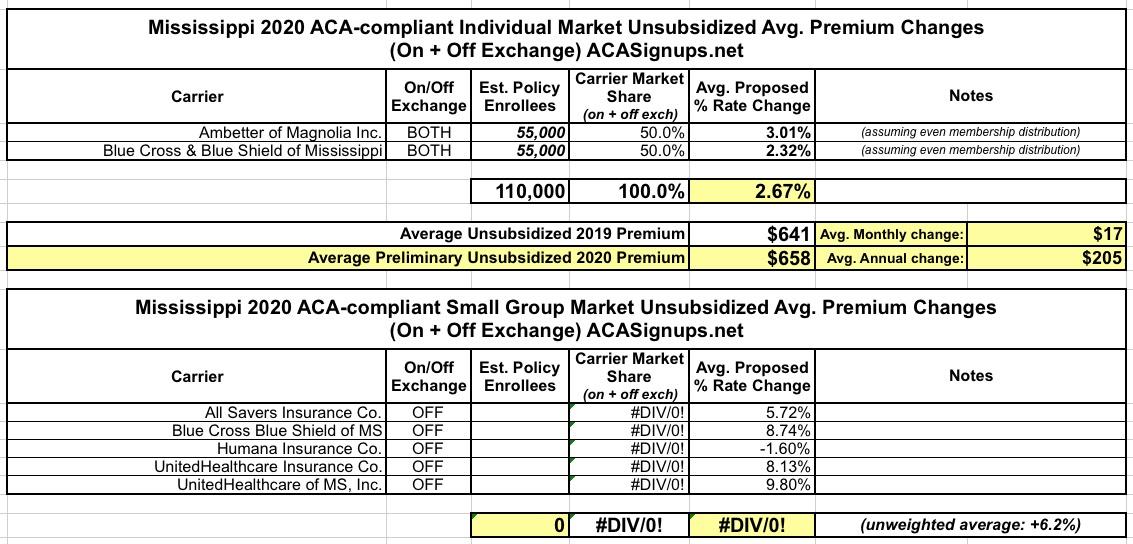

As a result, I have no idea what the relative market share is between the two and am assuming they're roughly even. Even if they aren't, the requested rate changes are so close it doesn't make much difference anyway (2.3% and 3.0%). If approved as is, unsubsidized Mississippians can expect to pay about $200 more total next year.

On the small group market, there's five carriers; again, I don't know the market share of any of them, so the unweighted average increase is 6.2% statewide.

Sen. Lindsey Graham (R-S.C.) said this week that Republicans would push to repeal ObamaCare if they win back the House and President Trump is reelected in 2020.

"If we can get the House back and keep our majority in the Senate, and President Trump wins reelection, I can promise you not only are we going to repeal ObamaCare, we're going to do it in a smart way where South Carolina will be the biggest winner," Graham said in an interview with a South Carolina radio station.

"We've got to remind people that we're not for ObamaCare."

As for "South Carolina will be the biggest winner", he's referring to this, his own "Graham-Cassidy" ACA replacement scheme:

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has ten different carriers participating in the individual market. MA (along with Vermont and the District of Columbia) has merged their Individual and Small Group risk pools for premium setting purposes, so I'm not bothering breaking out the small group market in this case.

Getting a weighted average was a bit tricky. On the one hand, only one or two of the rate filings included actual enrollment data. On the other hand, the Massachusetts Health Connector puts out monthly enrollment reports which do break out the on-exchange numbers by carrier. This allowed me to run a rough breakout of on-exchange MA enrollment. I don't know whether the off-exchange portion has a similar ratio, but I have to assume it does for the moment.

Huh. This is interesting...after a couple dozen states with near-flat or even reduced 2020 premiums, Louisiana is just the third state I've come across where the carriers are seeking double-digit rate increases for next year.

There's actually only 3 carriers offering individual market plans in Louisiana, but there's seven listings because two of the carriers have broken out their submissions into several different product lines. Overall, HMO LA, LA Health Service & Indemnity (Blue Cross Blue Shield of LA) and Vantage Health Plan are requesting average premium increases of 11.7% statewide.

I should note that there's also one odd listing (see second screenshot below), from UnitedHealthcare. It claims to be for off-exchange ACA-compliant individual market plans, but two things about it make no sense:

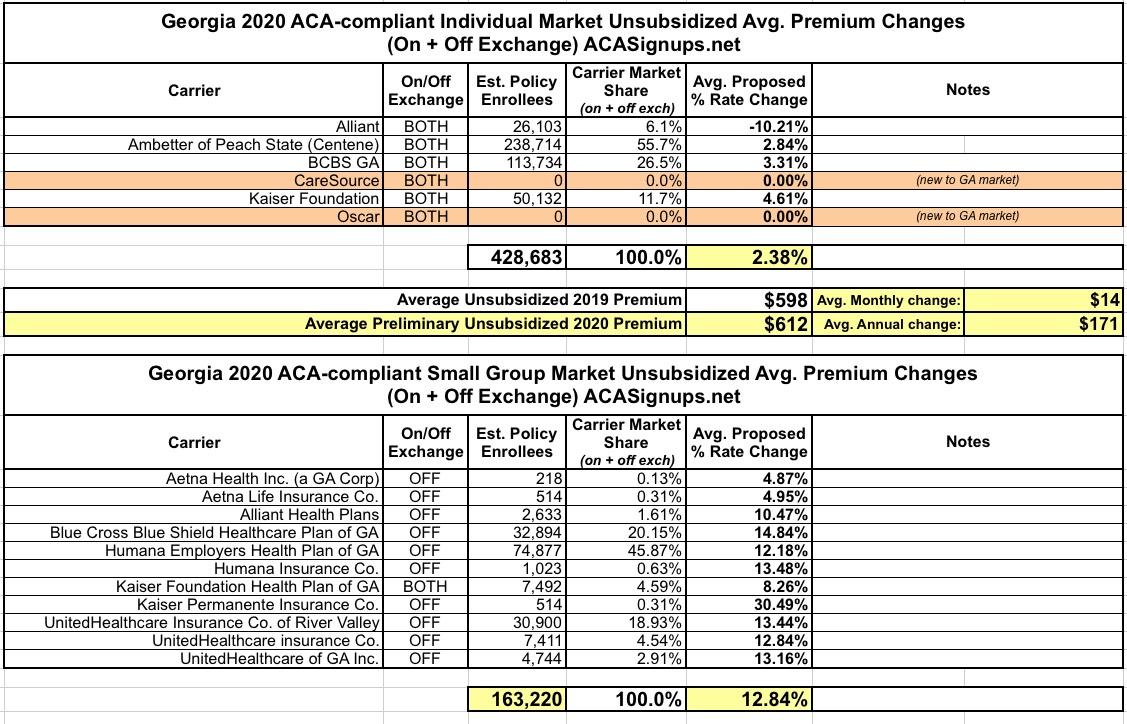

After several years with four carriers participating in their ACA individual market, the Peach State is gaining not one but two additional carriers this year: CareSource and Oscar are joining Alliant, Ambetter/Centene, Blue Cross Blue Shield and Kaiser. Unlike a lot of the states I've crunched numbers for recently, I was able to acquire hard enrollment numbers for every single Georgia carrier...including both the Individual and Small Group markets, which is a rarity this year!

Statewide, GA's individual market carriers are requesting average unsubsidized 2020 rate hikes of just 2.4%, while the small group carriers are looking for a 12.8% average increase: