Open Enrollment begins through Massachusetts Health Connector

BOSTON – Nov. 1, 2019 – The Massachusetts Health Connector started Open Enrollment this morning, making affordable coverage available to anyone in Massachusetts without health insurance, including lower-income people who can take advantage of low premiums and co-pays through the ConnectorCare program.

The Health Connector is Massachusetts’ state-based health insurance exchange, and provides health insurance to residents who do not get coverage through their employer. More than 97 percent of Massachusetts residents have health insurance, a result of the state’s 13-year old law which sought to ensure everyone in the Commonwealth has coverage.

ST. PAUL, Minn.—MNsure's seventh open enrollment period begins today, November 1. Minnesotans looking for coverage should visit MNsure.org to shop and compare plans. MNsure's seven-week open enrollment period runs until December 23, 2019.

Representatives from MNsure's Contact Center will be answering calls from 7 a.m. until 6 p.m. this evening. Extended hours can be found below.

Starting today, November 1st, the Seventh Annual ACA Open Enrollment Period is upon us! As I do every year, here's a list of important things to remember when selecting a health insurance policy. Some of these are the same every year and apply nationwide; others are specific to the 2020 enrollment period and/or to particular states.

1. DON'T MISS THE DEADLINE!

California actually launched Open Enrollment for 2020 on October 15th, but for the other 49 states (+DC) it starts on November 1st. The deadline for Open Enrollment is December 15th in most states for coverage starting January 1st, 2020, but eight states which operate their own ACA exchanges have extended deadlines:

Back in March I wrote an analysis of H.R.1868, the House Democrats bill which comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

There are three insurance carriers offering ACA-compliant individual market plans in West Virginia: CareSource, Highmark BCBS and Optum, although Optum has barely any enrollees at all, and the other two combined only total around 26,000 people in the state.

The final, approved average unsubsdized premiums for 2020 haven't changed from the requested rates--the weighted statewide average is a 6.7% increase.

Nothing terribly noteworthy about any of this, except that with that 6.7% increase, West Virginia has just taken the title for Most Expensive Obamacare Premiums in the Country, with average premiums averaging $990/month per enrollee, or nearly $12,000/year apiece.

This record was held by Wyoming last year (prior to that I believe Alaska had by far the highest rates in the country, until they instituted their ACA reinsurance waiver a few years back, which reduced full-price premiums by a good 25% or so).

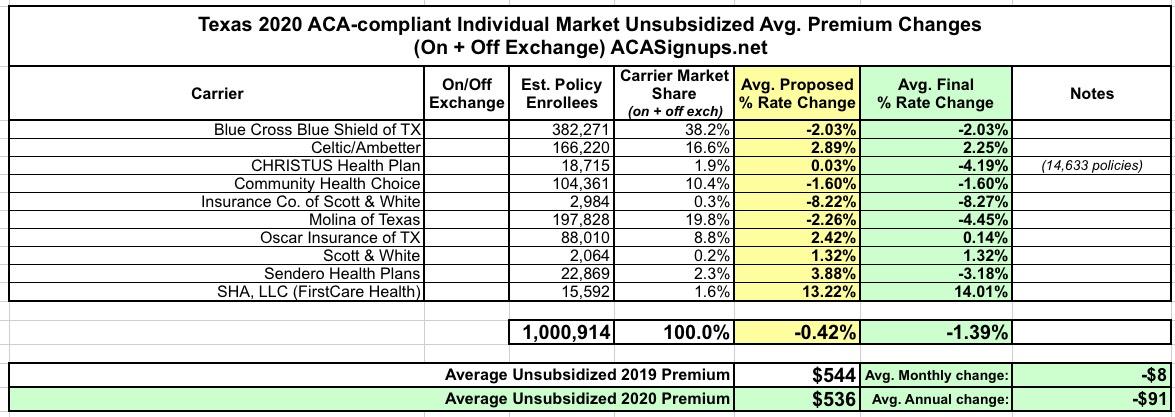

Back in mid-August, I plugged in the preliminary 2020 individual market rate change requests for unsubsidized enrollees in Texas. Unfortunately, at the time I only had hard enrollment data for some of the carriers, which meant I could only run a "semi-weighted" statewide average, which came in at +0.8%.

Since then, I've managed to find the enrollment data for the rest of the carriers as well...and yesterday CMS posted the final, approved 2020 rate changes, allowing me to run the complete, final, fully-weighted average. In the end rates in Texas are dropping by 1.4%:

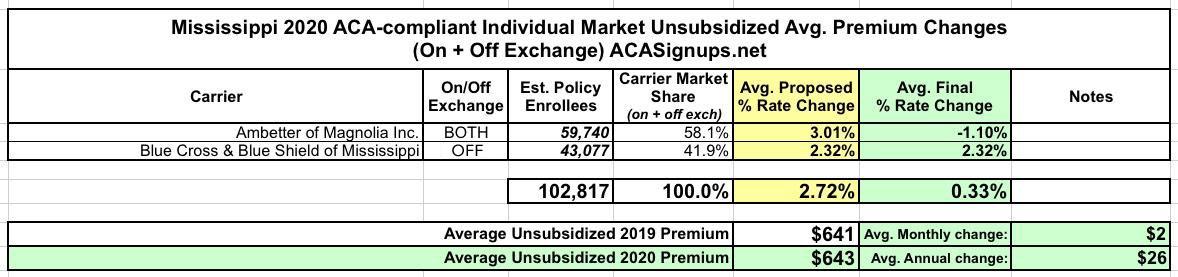

Mississippi once again has two carriers offering ACA-compliant individual market coverage in 2020: Ambetter of Magnolia, which holds 58% of the market, and Blue Cross Blue Shield with the other 42%. Earlier this year they were asking for average rate hikes of 3.0% and 2.3% respectively, but Ambetter's final/approved rates are coming in at a 1.1% reduction, bringing the overall average down to a mere 0.3% rate hike.

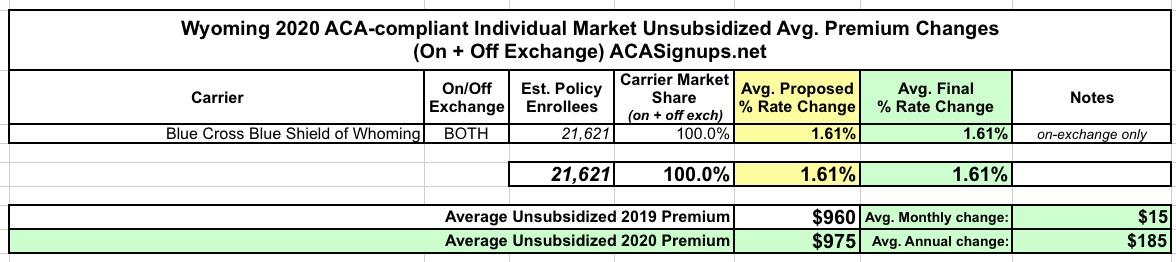

Not much to this one: Wyoming has just a single carrier selling ACA-compliant individual market policies to their 577,000 residents, Blue Cross Blue Shield...which is raising rates 1.6% on average for 2020. No change from their requested increase a few months earlier.

North Carolina has three individual market carriers in 2019. For 2020, that's increasing to four, as Bright Health Care is expanding into the NC market. The other three carriers (Blue Cross Blue Shield has a near monopoly at the moment) had requested average unsubsidized rate drops of 5.3% previously; in the end the final rates are dropping slightly more, to -5.6%.