The data below comes from the GitHub data repositories of Johns Hopkins University, execpt for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, August 15th (click image for high-res version):

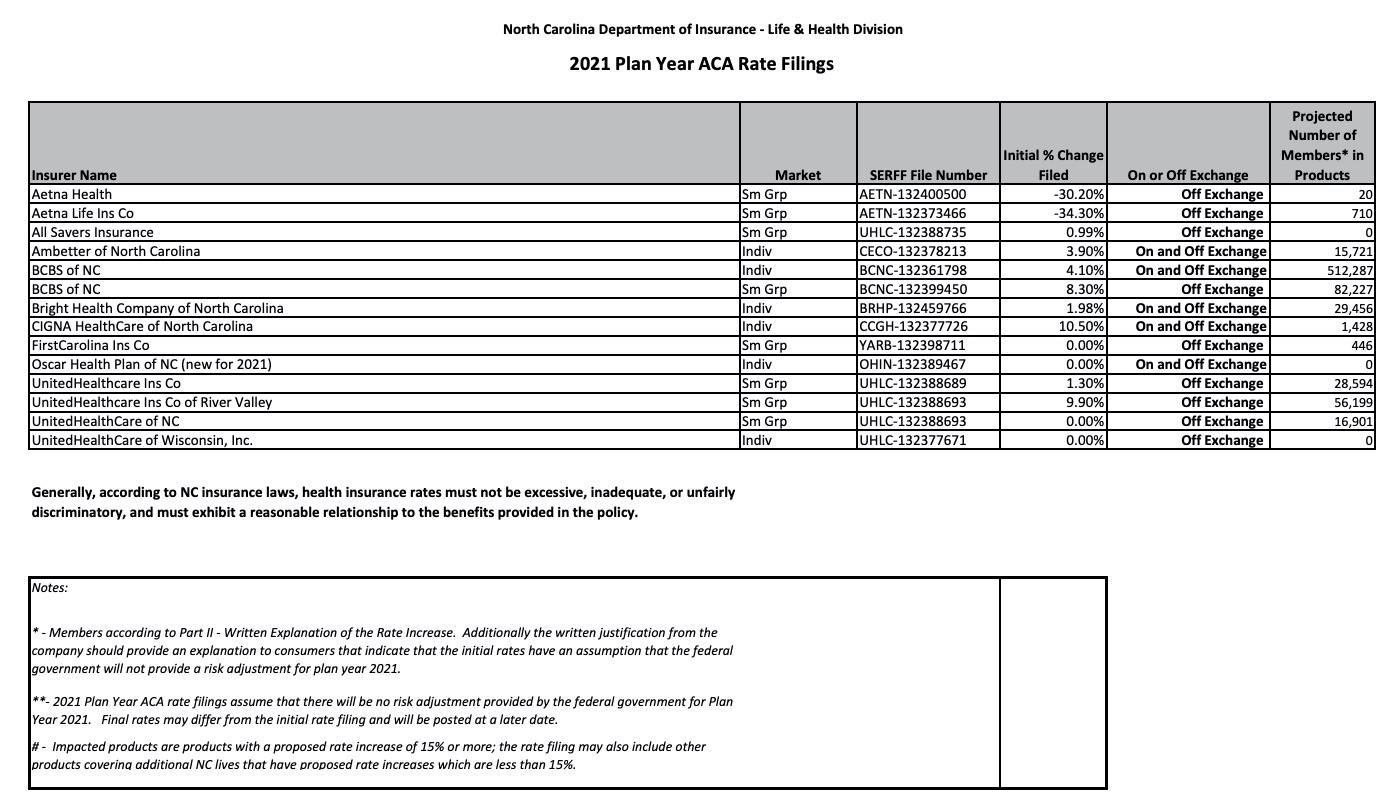

The good news is they include the number of people enrolled by each carrier in both markets, making it easy to calculate a weighted average, and th ey even include the SERFF tracking number for each.

The bad news is they don't include links to the actuarial memos, and even plugging the tracking numbers into the SERFF database only brings up the memos for three of the six carriers on the individual market...and of those, two of the three have been redacted (Oscar and Cigna), while the third (UnitedHealthcare) is brand-new to the North Carolina market anyway and therefore has no COVID-19 impact on their rate changes to speak of.

Are you turning 26 soon and still on your parent’s health insurance policy? Did you know that you will need to take action or you may no longer have health insurance? Don’t worry, you have options!

If you have a job that offers insurance, you can enroll in that coverage as turning 26—known as aging out—is considered a qualifying life event and will enable you to enroll in job-based coverage outside of your job’s open enrollment period.

Get covered through your school

If you are a college student, you may be able to enroll in a student health insurance plan through your school. Find out more

Nolan Finley is the conservative editorial page editor of The Detroit News.

Two weeks ago, he tweeted this out in response to criticism of the COVID-19 policy recommendations by himself and Michigan Republican legislative leadership:

Florida 20 million population, 6100 deaths. Michigan 10 million population, 6400 deaths. https://t.co/O1tNoyWwB0

Let's take a look at the data, shall we? Here's a graph of official COVID-19 positive test cases and fatalities per capita for both Michigan and Florida. Cases are per 1,000 residents; deaths are per 10,000 in order to make the trendlines more visible:

As I noted last year, the Nevada Insurance Dept. website is both helpful and frustrating when it comes to tracking down the type of data that I need. On the one hand they make it very easy to view the individual & small group market rate filing summaries: Carrier names, markets, sumission dates, status, effective dates and most importantly, the proposed and approved average rate changes are all easily found.

On the other hand, they don't actually link to the filing memos or URRT forms, which means I can't find the actual effectuated enrollment numbers for each carrier, the impact of COVID-19 on each carrier's request or other noteworthy info about the filings. Oddly, they do include the SERFF tracking numbers...except that plugging those into the SERFF database still doesn't bring anything up, which kind of defeats the point.

Fortunately, the NV DOI does provide the weighted average of the entire market and COVID-19 impact elsewhere. I've also been able to piece together the total market enrollment (both on & off-exchange) using some other public data.

With recent reports illustrating the growing number of uninsured Americans across the country, MNsure is reminding Minnesotans that there are options. For those who have lost their health insurance, seen a change in income, or experienced a qualifying life event, enrollment opportunities may be available.

"The last couple of months has brought tremendous uncertainty to many families across the state," said MNsure CEO Nate Clark. "It's important that Minnesotans know there are enrollment opportunities available if they lose their health insurance. MNsure is here to help."

Since the start of the COVID-19 pandemic, more than 100,000 Minnesotans have come through MNsure to find health insurance coverage.

For new customers, you may be eligible to enroll if:

I've acquired the preliminary 2021 rate filings for Georgia's individual and small group market carriers. There were two filings submitted for many of the carriers because of a (since delayed) ACA Section 1332 waivier submission; the carriers submitted one in case the waiver was approved and a second if it wasn't. Since the process has been delayed, however, the no-waiver filing is the one which is relevant.

As you can see in the tables at the bottom of this entry, the overall weighted rate change requested by individual market carriers in Georgia is a 1.3% reduction, which would have been more like a 2.3% drop if not for the COVID-19 factor, according to the carriers. The small group market carriers are requesting an 11.1% average increase, which is unusually high these days. I haven't reviewed all the memos for the sm. group market to see what they're pinning on COVID-19, however.

Here's what the indy market carriers have to say about the COVID-19 factor in their 2021 filings:

The data below comes from the GitHub data repositories of Johns Hopkins University, execpt for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, August 8th (click image for high-res version):

I don't often swear on this site (and almost never in the lede of the blog post, but this is the most sickening bit of gaslighting I've seen in awhile, which is saying something for the Trump Administration.

About an hour or so ago, Trump held a "press conference" in which he announced that he's supposedly signing an executive order to do exactly what the Patient Protection & Affordable Care Act, which he's currently suing to have struck down, ALREADY DOES.

So how is this being reported by certain "news media" outlets? Let's take a look:

Back on March 10th, the Washington HealthPlanFinder became the first state-based ACA exchange/marketplace to formally create an official COVID-19 Special Enrollment Period, which was originally scheduled to have a deadline of April 8th.

Since that time, nearly every other state-based ACA exchange (all of them except for Idaho) has done likewise. Some of them required some sort of verbal or written attestation of thier eligibility status, while others didn't, but all of them were wide open to any uninsured resident who would normally be eligible to enroll during the official Open Enrollment Period.

The deadlines for the "open" COVID-19 SEP varied by state...but most of them ended up extending them out as that deadline approached. In some cases, they bumped it out again...and again...and yet again, as it became increasingly clear that the deadly pandemic isn't going away anytime soon.