That sound you heard was an Insurance Carrier-Shaped Hole being broken through the wall.

Wed, 07/19/2017 - 5:48pm

I actually used this exact same headline seven months ago, and now we've apparently come full circle and are right back where we started:

The New York Times, December 2nd:

“The idea that you can repeal the Affordable Care Act with a two- or three-year transition period and not create market chaos is a total fantasy,” said Sabrina Corlette, a professor at the Health Policy Institute of Georgetown University. “Insurers need to know the rules of the road in order to develop plans and set premiums.”

Having talked to a number of CEOs & states, @SabrinaCorlette is right, if not understating.https://t.co/Ri5TtkHz7Z

— Andy Slavitt (@ASlavitt) December 3, 2016

I'm stuck in a loop of:

1. Reading this article... https://t.co/QjH2Evfldw

— Aisling McDonough (@AislingMcDL) December 3, 2016

Everything I said last December is still true today. The only edits below are a couple of tweaks (changing 20 million to 18 million, a 3-year delay to only 2 years, and 'Paul Ryan' to 'Mitch McConnell'):

Let's get this straight: I am no fan of the private, profit-based insurance industry. I have little sympathy for the CEOs who get paid up to $17 million per year. I'm on the record as being a single payer advocate (or at least, something much closer to single-payer than we have now).

HOWEVER, at the moment, there are around 18 million people who are:

- Under 65 years old (ie, they don't qualify for Medicare), but...

- Earn more than 138% of the Federal Poverty Line in 31 states or over 100% FPL in the other 19 (ie, they don't qualify for Medicaid), and...

- Aren't in a position to receive healthcare coverage via their employer (ie, they don't qualify for large or small-group coverage)...

...whose only viable option for comprehensive healthcare coverage happens to be the private individual/non-group market. And until that changes, private, profit-based health insurance carriers are pretty much what those people (myself included) have to contend with.

So, for the moment, let's forget about whether or not the Insurance Companies are Evil® or not, because that's kind of irrelevant at the moment. You may think that they should stick around the individual market for the Good of Humanity, etc etc...but the bottom line is...the bottom line. If a given insurance carrier believes that offering policies on the individual market (whether on or off the ACA exchanges) will be profitable, they'll do so. If they don't think it will be profitable, they won't. It's that simple.

The only caveat to this is that they might be willing to stick around and eat some amount of losses for a few years while the market settles down and stabilizes...but they'll only do this if they're reasonably sure of profits from the individual market in the foreseeable future.

Some carriers happened to get it right early on, and have been making profits off the ACA exchanges already, such as Centene, Molina and Florida Blue.

Some carriers gave it a shot for a few years, lost a bunch of money and decided to largely pull up stakes already, such as UnitedHealthcare, Aetna and Humana.

Finally, there are other carriers which may have lost money the first few years but which seem to be turning things around, such as Blue Cross Blue Shield of North Carolina.

The point is that as ugly as this year's 25% average unsubsidized rate hikes on the indy market may prove to be, there's quite a bit of evidence that the tide has finally started to turn, and that once we get over the 2017 hump, the market should stabilize, the current carriers should become far more likely to turn a profit, and the carriers which bailed may be encouraged to dip their toes back in the water.

The moment that the ACA is repealed, however...whether partially or fully, and whether there's a "2 year delay" or not...all of that becomes moot.

Again, look at this from the perspective of an insurance carrier CEO. Let's say you're participating in all 5 markets: Managed Medicare, Managed Medicaid, Large Group, Small Group and Individual.

Let's say you're making money in 4 of them. For the individual market, you've been losing money, but you've been biding your time for 4 years now, holding your tongue, patiently waiting for the ACA dust to settle. You start to see the light at the end of the tunnel; this final rate hike seems to have done the trick. Next year you'll break even; in 2018, you might even turn a profit in this division as well! Yay!

And then...

REPEAL.

Oh, don't worry, Mitch McConnell says; the exchanges will still be around for another 2 years...before we pull the plug on them permanently.

Really? Seriously?

Would you be willing to keep dealing with the hassles for another 2 years when you know it's all gonna be for nothing at the end of that period anyway?

Some carriers might, but I strongly suspect that most of them will find this to be the last straw, cut their losses and bail...as soon as 2018.

And let's be very clear about this: If the Republican Party and the Republican President do indeed repeal the Affordable Care Act--either partially or fully, and with either immediate effect or a 3-year delay, the responsibility for the disruption to the market, tens of millions of people losing their coverage and confusion all around will fall completely on them, and no one else.

Well, just an hour or so ago, the Congressional Budget Office released their score of the Senate GOP's updated version of their old 2015 ACA repeal bill. Almost nothing has changed at their end either, besides the implementation dates being nudged forward a bit. The only substantive change I see so far is that, like both the AHCA and BCRAP bills, the "Obamacare Repeal Reconciliation Act" (yes, that's right: They're actually using the word "Obamacare Repeal" in the legal title, even though there's no such law on the books) does actually appropriate CSR reimbursements for 2 years (before, again, killing the program entirely).

So, what's the bottom line from the CBO this time around? Pretty much exactly what they said last winter, with a few minor tweaks:

CBO and JCT estimate that enacting the legislation would affect insurance coverage and premiums primarily in these ways:

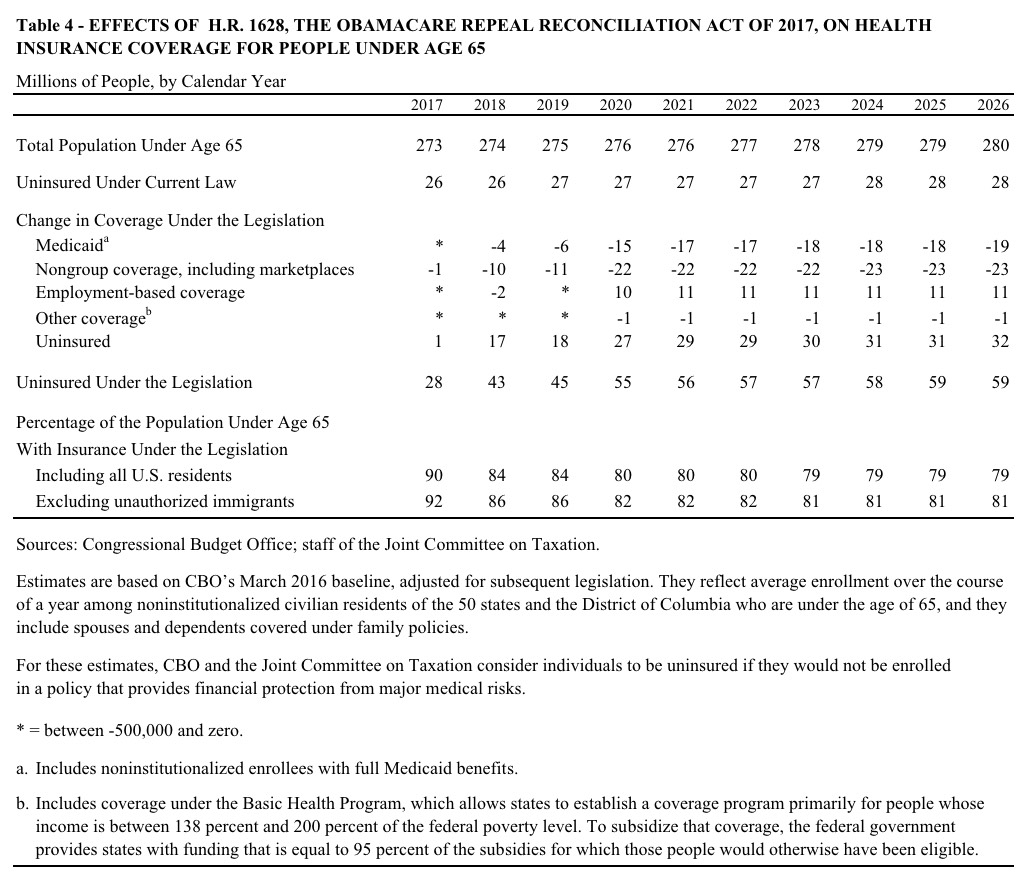

- The number of people who are uninsured would increase by 17 million in 2018, compared with the number under current law. That number would increase to 27 million in 2020, after the elimination of the ACA’s expansion of eligibility for Medicaid and the elimination of subsidies for insurance purchased through the marketplaces established by the ACA, and then to 32 million in 2026.

- Average premiums in the nongroup market (for individual policies purchased through the marketplaces or directly from insurers) would increase by roughly 25 percent—relative to projections under current law—in 2018. The increase would reach about 50 percent in 2020, and premiums would about double by 2026.

In CBO and JCT’s estimation, under this legislation, about half of the nation’s population would live in areas having no insurer participating in the nongroup market in 2020 because of downward pressure on enrollment and upward pressure on premiums. That share would continue to increase, extending to about three-quarters of the population by 2026.

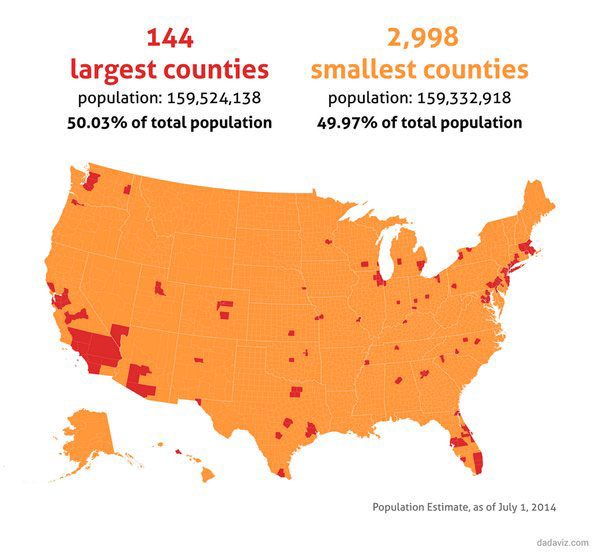

For the record: According to Pew Research, half of all Americans live in just 144 counties, while the other half live in the remaining 2,998 counties. Since it's the rural counties which already have the biggest problems with a lack of competition in the individual marketplace, it follows that under the "Repeal/Delay" scenario, the CBO is basically saying that 95% of all counties nationally wouldn't have any carrier available in 2020.

It's important to reiterate that the "25% rate hike" would be on top of whatever rates would be increasing otherwise. Ironically, since ORRA (yes, that's the new acronym), like AHCA and BCRAP, would fund CSR payments for 2 years, premium hikes which are currently looking to be roughly 34% at the moment would "only" increase by "slightly" more than that next year (without CSRs, rates would go up around 19% on top of the 15% caused by other reasons; under ORRA you'd be looking at 15% + 25% = around 40% next year).

I know there's been a lot of debate/controversy about the "net coverage loss by 2026" number, since the CBO keeps using March 2016 as their baseline instead of January 2017. They address that here:

Use of the March 2016 Baseline

On the basis of consultation with the budget committees, CBO and JCT measured the costs and savings in this estimate relative to CBO’s March 2016 baseline projections, with adjustments for legislation that was enacted after that baseline was produced. That approach is not unusual: The budgetary effects of reconciliation legislation are typically estimated relative to the baseline that underlies the budget resolution that specified the reconciliation instructions and that was the basis for the deficit reduction goals stated in the resolution. Also, using the March 2016 baseline facilitates comparison because it has been used by CBO and JCT for cost estimates for all pieces of legislation related to the budget reconciliation process for 2017, including this one. The agencies have not had time to undertake a follow-on analysis of the effects of this legislation under the agencies’ most recent baseline.

Having said that, yes, if the CBO was to use January 2017 as their baseline, the 2026 net loss total would likely be a few million fewer (perhaps 28 million instead of 32 million. This is because the individual market is a couple million smaller today than the CBO had projected earlier, so it's reasonable to expect it to be a few million smaller 9-10 years down the road as well under current law. However, it's also worth noting that part of the reason why it's smaller is because of GOP sabotage of the ACA exchanges, so that's a bit of a disingenuous argument. Basically, the CBO made the naive mistake of assuming that the Republican Party would stop being jackasses going forward, which obviously was a misjudgment.

I should also note that this is especially true when it comes to Medicaid expansion--one reason the CBO's Medicaid expansion loss numbers are as high as they are is that they keep assuming that, if the ACA isn't repealed, most of the non-expansion states will eventually come around (i.e., their GOP governors/legislators will stop being douchnozzles). The GOP's argument on this issue is literally "that's never gonna happen no matter what, so you can't count people as "losing" Medicaid when we wouldn't ever provide it to them in the first place anyway!"

OK, so what would and wouldn't actually be repealed/changed, and when?

The largest budgetary effects of enacting the legislation would stem from:

- Repealing the optional expansion of eligibility for Medicaid established in the ACA, beginning in 2020;

- Repealing subsidies for health insurance coverage obtained through the marketplaces beginning in 2020 and, prior to that year, eliminating the limitation on the amount people would have to repay if the premium tax credit they received during the year exceeded the allowed amount based on their actual income;

- Beginning upon enactment, eliminating penalties associated with the requirements that most people obtain health insurance coverage (also known as the individual mandate) and that large employers offer their employees health insurance coverage that meets specified standards (also known as the employer mandate), while keeping those requirements in place; and

- Repealing many of the provisions of the ACA that increase federal tax revenues (apart from the effect of the provisions related to insurance coverage) and delaying the federal excise tax imposed on some health insurance plans with high premiums so that it would take effect in 2026.

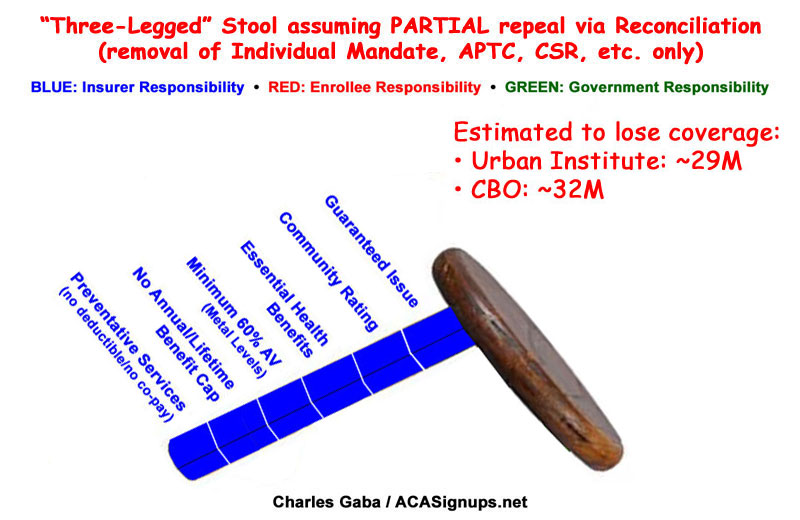

Whoa. That one's huge...Medicaid expansion and tax credits would be killed off starting in 2020...but the individual mandate would be repealed IMMEDIATELY.

In other words, this would rip away one leg of the 3-legged stool right away, and a second one 2 years later...while leaving the third in place.

Upon enactment, other parts of the legislation that affect the budget would:

- Repeal reductions to state allotments for Medicaid payments to hospitals that treat a disproportionate share of uninsured or low-income patients;

- Increase the amount of funding authorized for and appropriated to the Community Health Center Fund and for grants to states to address substance abuse; and

- Prohibit federal funds from being made available, for one year, to certain entities that provide abortions.

Yup. They're gonna defund Planned Parenthood for a year, for no particular reason other than they can't stand Planned Parenthood since a completely separate division of the organization (100% separately funded) does provide abortion services. Which are, you know, legally protected medical procedures

In addition, in later years, the legislation would do the following:

- Eliminate the Prevention and Public Health Fund, beginning in 2019, and

- Terminate the enhanced federal matching rate for personal care services and supports provided under the Community First Choice Act, beginning in 2020

Because as long as you're doing horrible things, what the hell, might as well go for broke.

Let's take a look at the CBO's projections for next year (2018) specifically, since that's obviously pretty important politically with the midterms coming up and all:

Estimated Changes Starting in 2018.

Following enactment but before the Medicaid expansion and subsidies for insurance purchased through the marketplaces were eliminated, the effects of this legislation on insurance coverage and premiums would stem primarily from repealing the penalty associated with the individual mandate.

Effects on Insurance Coverage.

In 2018, by CBO and JCT’s estimates, about 17 million more people would be uninsured under this legislation than under current law. 3 That increase in the uninsured population would consist of about 10 million fewer people with coverage obtained in the nongroup market, roughly 4 million fewer people with coverage under Medicaid, and about 2 million fewer people with employment-based coverage. In 2018, an estimated 84 percent of all U.S. residents under age 65 would be insured, compared with 90 percent under current law.

Although most of those reductions in coverage would stem from repealing the penalty associated with the individual mandate, CBO and JCT also expect that insurers in some areas would leave the nongroup market in 2018. They would be leaving in anticipation of further reductions in enrollment and higher average health care costs among enrollees who remained after the subsidies for insurance purchased through the marketplaces were eliminated. As a consequence, roughly 10 percent of the population would be living in an area that had no insurer participating in the nongroup market.

...which is exactly what I wrote about last December. If you think carriers have been abandoning the market up until now, just wait and see the stampede if this garbage bill becomes law.

In the nongroup market, some people would choose not to have insurance partly because they choose to be covered by insurance under current law to avoid paying the penalty. And, under this legislation, without the mandate penalty, some people would forgo insurance in response to the higher premiums that CBO and JCT project would be charged. Insurers would still be required to provide coverage to any applicant, and they would not be able to vary premiums to reflect enrollees’ health status or to limit coverage of preexisting medical conditions. Those features are most attractive to applicants with relatively high expected costs for health care, so CBO and JCT expect that repealing the individual mandate penalty would tend to reduce insurance coverage less among older and less healthy people than among younger and healthier people. Thus, the agencies estimate that repealing that penalty, taken by itself, would increase premiums in the nongroup market.

More to come after dinner...

UPDATE: OK, lessee, what else...

Under current law, the penalty associated with the individual mandate applies to some Medicaid-eligible adults and children. (For example, it applies to single individuals with income above about 90 percent of the FPL.) In addition, some people apply for coverage in the marketplaces because of the penalty and turn out to be eligible for Medicaid. And some who are not subject to the penalty think they would be if they did not enroll in Medicaid. The agencies do not expect that, with the penalty eliminated under this legislation, people enrolled in Medicaid would disenroll. However, among people who would become eligible for Medicaid under the legislation or who would need to recertify their eligibility, the proportion of people who enrolled in the program would, by CBO and JCT’s expectations, be lower—closer to the proportions observed for those groups prior to the institution of the penalty.

This is an important clarification, and helps clear up one of the criticisms of the CBO's prior scores: They aren't saying that they think 4 million current Medicaid enrollees would drop from the Medicaid roles due to the mandate being repealed, but they do think that several million people who otherwise would have JOINED the Medicaid roles would no longer do so. I actually think that 4 million the first year and 6 million the second seems a bit high, but the principle makes sense.

Under current law, the prospect of paying the employer mandate penalty tips the scale for some businesses and causes them to decide to offer health insurance to their employees. Thus, eliminating that penalty would cause some employers to not offer health insurance. Similarly, the demand for insurance among employees is greater under current law because some employees want employment-based coverage so that they can avoid paying the individual mandate penalty. Eliminating that penalty would reduce such demand and would cause some employers to not offer coverage or some employees to not enroll in coverage they were offered, CBO and JCT estimate.

Again, I actually support eliminating the employer mandate penalty as the last item in my "If I Ran the Zoo" list...but only as part of a strategy to move more people onto the individual market, including the full tax credit/mandate penalty structure there. That's a very different thing.

Of course, 2020 is when the shit would really hit the fan:

The estimated increase of 32 million people without coverage in 2026 is the net result of roughly 23 million fewer with coverage in the nongroup market and 19 million fewer with coverage under Medicaid, partially offset by an increase of about 11 million people covered by employment-based insurance. By CBO and JCT’s estimates, 59 million people under age 65 would be uninsured in 2026 (compared with 28 million under current law), representing 21 percent of everyone under age 65. By 2026, fewer than 2 million people would be enrolled in the nongroup market, CBO and JCT estimate

Yup. Exactly what happened to New York's individual market a decade ago. I read one article saying that prior to the ACA exchanges launching, NY's entire individual market was down to something like 10,000 people (out of a total population of nearly 20 million).

Effects on Market Stability.

According to the agencies’ analysis, eliminating the penalty associated with the individual mandate and the subsidies for insurance while retaining the market regulations would destabilize the nongroup market, and the effect would worsen over time. The ACA’s changes to the rules governing the nongroup health insurance market work in conjunction with the mandate and the subsidies to increase participation in the market and encourage enrollment among people of different ages and health statuses. But eliminating the penalty for not having health insurance would reduce enrollment and raise premiums in the nongroup market. Eliminating subsidies for insurance purchased through the marketplaces would have the same effects because it would result in a large price increase for many people.

"work in conjunction with the mandate and the penalties"...in other words, again, rip away 2 legs of the 3-legged stool and it topples over.

Not only would enrollment decline, but the people most likely to remain enrolled would tend to be less healthy (and therefore more willing to pay higher premiums). Thus, average health care costs among the people retaining coverage would be higher, and insurers would have to raise premiums in the nongroup market to cover those higher costs. CBO and JCT expect that enrollment would continue to drop and premiums would continue to increase in each subsequent year.

Classic death spiral.

Leaving the ACA’s market regulations in place would limit insurers’ ability to use strategies that were common before the ACA was enacted. For example, insurers would not be able to vary premiums to reflect an individual’s health care costs or offer health insurance plans that exclude coverage of preexisting conditions, plans that do not cover certain types of services (such as maternity care), or plans with very high deductibles or very low actuarial values (plans paying a very low share of costs for covered services).

Again: These are good things, but only if provided "in conjunction with" the two legs they just tore away.

To be honest, the one number which I find the biggest head-scratcher is the CBO's projections that employer-sponsored coverage would be 10-11 million people higher than under the ACA starting in 2020. They really don't talk about their reasoning on this one...I searched through the entire PDF and the only specific reference to group coverage changes was when they talked about it dropping by 2 million initially. There's no mention at all of why they're so sure 10-11 million more people would be covered via their employer after the employer mandate is dropped. Huh.

Anyway, I'll leave it at that; I'm sure folks have already read plenty of other Hot Takes on the CBO score, and they're supposedly going to be releasing the "Cruzified" BCRA 2.0 score tomorrow as well, so we'll see...

Advertisement